Beyond the Ranking: Why Taiwan and South Korea are Not Direct Peers to India

India’s recent slide in global market-cap rankings has triggered widespread investor anxiety, but the reality is more nuanced. A deep dive into sectoral divergences reveals why this is a tactical rotation rather than a structural failure.

Photo by Monstera Production on Pexels

Beyond the Ranking: Why Taiwan and South Korea are Not Direct Peers to India

For the Indian retail investor, the past seven days have felt like a high-stakes financial whiplash. In a rapid succession that sent shockwaves through social media forums, India slipped from the world’s fifth-largest stock market to seventh, being overtaken by both Taiwan and South Korea in a single week. For a nation accustomed to the "India Growth Story" narrative, the optics are undeniably jarring. But beneath the headlines lies a reality defined not by structural collapse, but by a massive, global rotation of capital into the AI hardware supply chain—a sector where India and its peers are playing fundamentally different games.

The Optical Illusion of the Ranking Slide

Market capitalization is a volatile metric, and often a misleading one. When we measure global rankings, we are essentially looking at a snapshot of asset prices denominated in USD. Consequently, when the INR experiences even slight depreciation against the dollar, the USD-denominated market cap of Indian firms drops automatically, even if the underlying company performance remains unchanged.

Furthermore, market cap acts as a popularity index rather than a barometer of national economic health. It reflects current sentiment and liquidity, not the long-term compounding potential of a country's GDP. The recent "shock" is a direct function of the aggressive AI hardware rally, which has funneled billions into the semiconductor-heavy indices of Taiwan and South Korea, leaving markets like India—which rely on diverse, consumption-led growth—temporarily on the sidelines.

""India Hit By A SHOCK Again: After Taiwan, South Korea Surpasses In Stock Market Ranking, Slip To 7 Position Within A Week." — u/FinancialAnalyst, r/IndianStreetBets

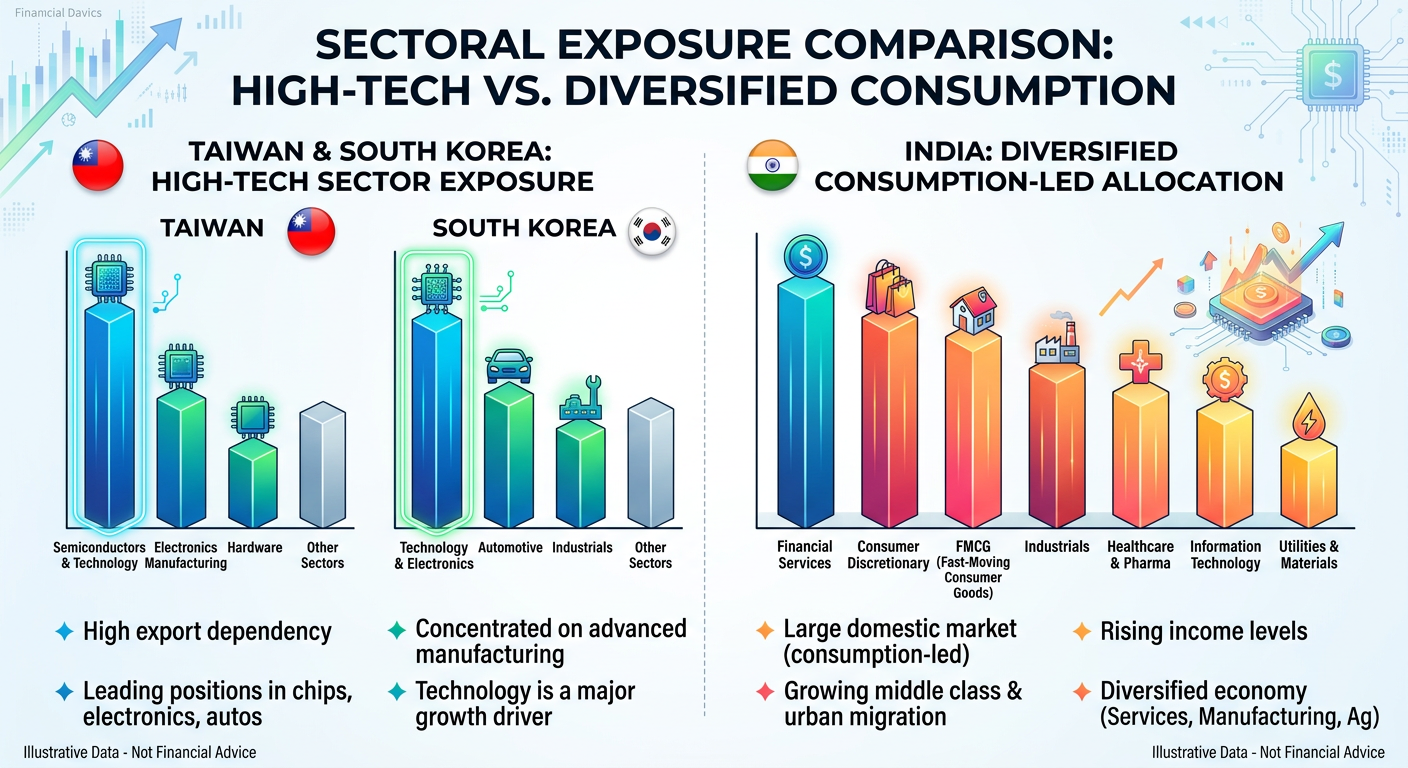

Structural Divergence: Semiconductors vs. Consumption

To compare India’s Nifty 50 to the Taiwan Stock Exchange or the KOSPI is to compare apples to silicon. The latter two are effectively proxies for the global semiconductor industry. Their indices are heavily concentrated in giants like TSMC, which are currently enjoying a massive valuation premium due to the global frenzy over Nvidia and AI-centric computing.

India’s market, by contrast, is a reflection of a massive, growing domestic economy. Our top performers aren't chip manufacturers; they are banks, consumer goods companies, and infrastructure conglomerates. When global capital chases the "AI Alpha," it naturally rotates out of broad-based, consumption-heavy markets and into the hardware-heavy tech hubs. This is not an abandonment of India; it is a tactical reallocation of capital toward the highest beta, tech-centric sectors.

FII Exodus: Tactical Profit Taking or Long-term Exit?

Is the exit of Foreign Institutional Investors (FIIs) a sign of structural distrust? The evidence suggests otherwise. Much of the current outflow is a result of "valuation exhaustion" in the Indian mid-cap and small-cap space. After a sustained bull run, many Indian stocks reached unsustainable P/E multiples, making them prime candidates for profit-taking by global funds looking to rebalance their portfolios.

Crucially, the Indian market now benefits from a robust 'domestic floor.' Sustained inflows from Domestic Institutional Investors (DIIs) and the ever-growing retail SIP (Systematic Investment Plan) culture have created a buffer that didn't exist a decade ago. This domestic liquidity has prevented a catastrophic freefall, turning what could have been a crash into a controlled, necessary valuation correction.

"India's Stock Market Drops to 7th Globally as Foreign Investment Hits Decade Low. Is this the end of the India premium, or just a breather before the next leg up?" — u/MacroWatcher, r/IndiaInvestments

India’s Play in the AI Ecosystem

While India may not be building the chips, it is becoming the essential "picks-and-shovels" layer of the AI economy. Our growth is moving toward data centers, power infrastructure, and cooling systems—the physical, terrestrial requirements of a digital-first global economy.

Investors would do well to look past the chip-maker dominance of our East Asian peers. While their indices are tied to the cyclical nature of semiconductor hardware demand, India’s exposure is built on durable, long-term capital expenditure. The "India Story" isn't about competing with Taiwan for semiconductor supremacy; it is about building the infrastructure that hosts the services, software, and scale that these chips ultimately enable.

The Bottom Line

Market-cap rankings are transient; economic fundamentals are not. The shift in ranking is an optical consequence of the AI-driven tech cycle rather than a failure of India’s economic trajectory. For the 22-40 demographic, the current volatility is a reminder that market cycles are inevitable, but the structural demographic dividend and the domestic savings floor remain the most vital metrics for long-term wealth creation. Don't let the leaderboard dictate your investment horizon.