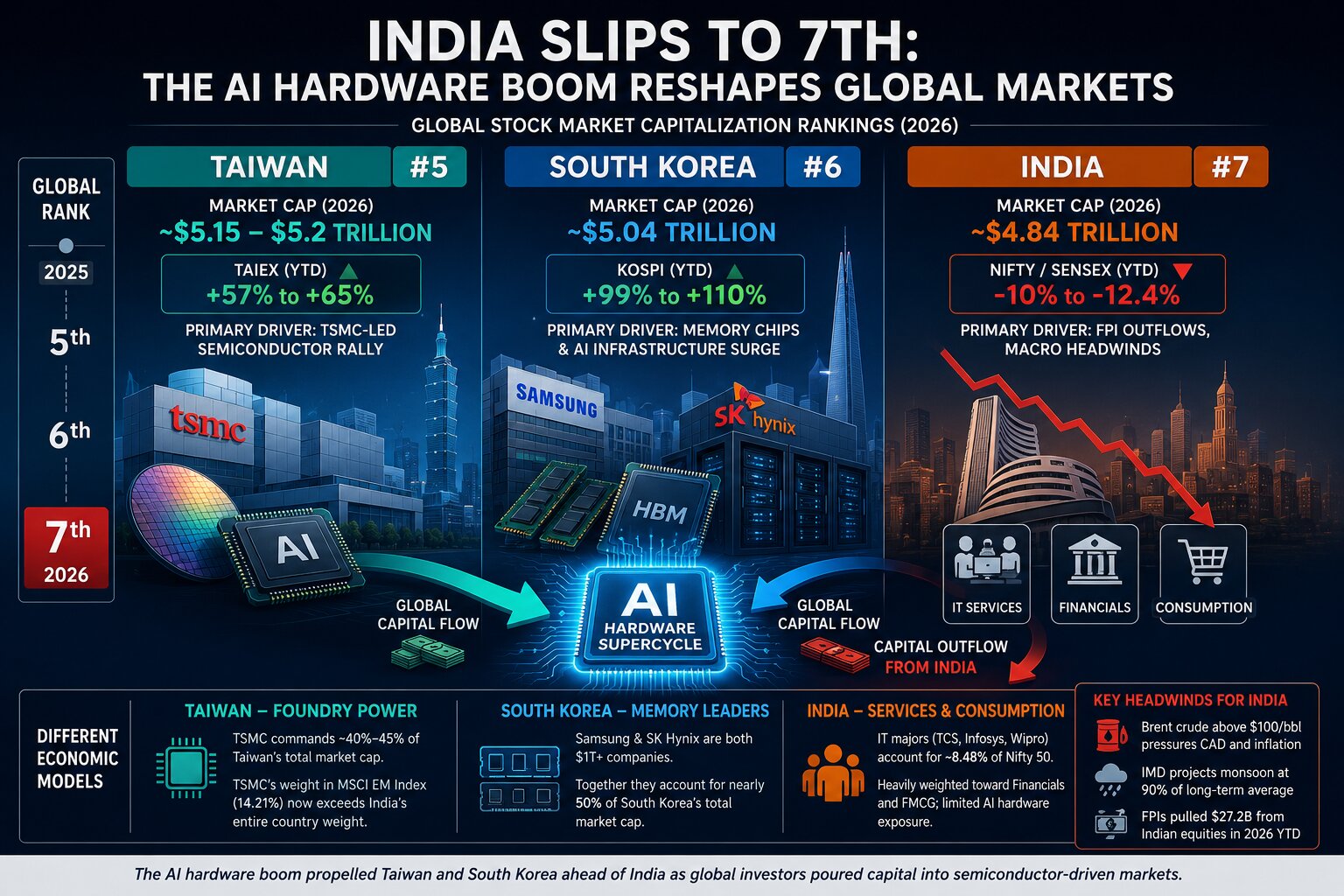

India Slipped From 6th to 7th in Global Market Capitalization Rankings

As India slips to 7th in global market capitalization, investors are asking if our traditional reliance on finance and consumer goods is leaving us behind. With South Korea and Taiwan surging on the back of the semiconductor AI-boom, the debate over a structural pivot for the Indian economy has never been more urgent.

Photo by Markus Spiske on Pexels

Beyond the Ranking: Why India's Tech-Light Portfolio Is Losing the AI Race

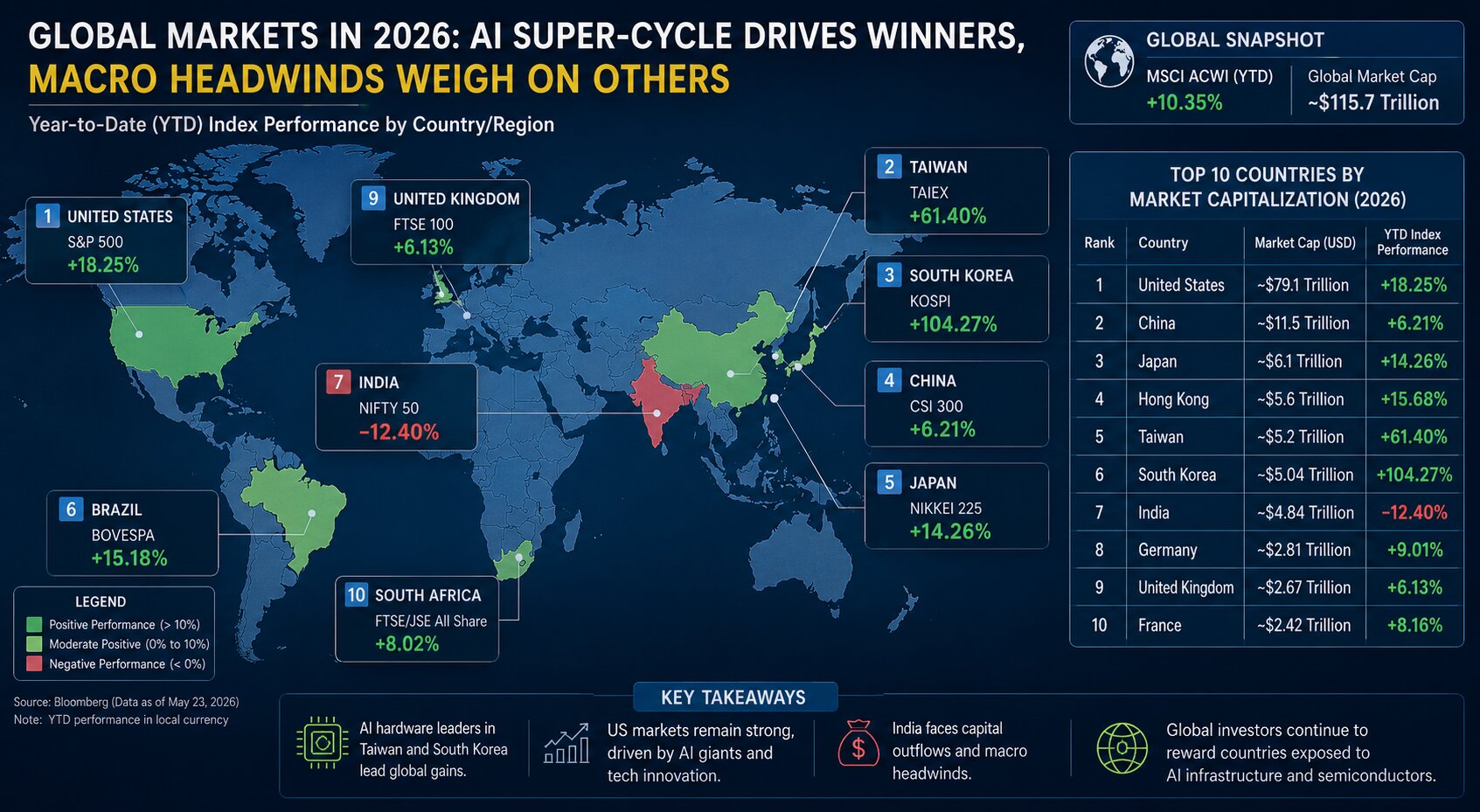

India has officially slipped from 5th to 7th place in global stock market capitalization rankings, overtaken first by Taiwan and then by South Korea. While the headline may appear alarming, the underlying story is less about India's economic weakness and more about a historic shift in global capital allocation during the AI hardware super-cycle.

The ranking reversal reflects a collision between two fundamentally different economic models. On one side are economies deeply embedded in semiconductor manufacturing and AI infrastructure. On the other is India, whose market remains heavily concentrated in financial services, consumer businesses, and IT services.

The Global Reversal: How India Lost Ground

Recent market capitalization data highlights the scale of the divergence.

| Country / Region | Market Capitalization (2026) | YTD Market Performance | Primary Driver |

|---|---|---|---|

| United States | ~$79.1 Trillion | Nasdaq +21% | Nvidia-led AI boom |

| Taiwan | ~$5.15–5.2 Trillion | TAIEX +57% to +65% | TSMC-driven semiconductor rally |

| South Korea | ~$5.04 Trillion | KOSPI +99% to +110% | Memory-chip and AI infrastructure surge |

| India | ~$4.84 Trillion | Sensex/Nifty -10% to -12.4% | FPI outflows and macro headwinds |

The shift occurred rapidly as global investors rotated capital away from consumer and service-oriented economies toward markets that own the critical hardware powering artificial intelligence.

This is not necessarily a story of domestic collapse. Rather, it is a reflection of where global investors believe the greatest AI profits will be generated over the next decade.

""After Taiwan, now South Korea overtook India to become the world's sixth biggest stock market. India slips to 7th position." — r/IndiaInvestments

The Extreme Concentration of the AI Trade

One of the most striking aspects of the current rally is how heavily concentrated it has become.

Taiwan: The Foundry Advantage

Taiwan's market surge is largely synonymous with TSMC's rise. The semiconductor giant has expanded its valuation beyond $2 trillion, accounting for roughly 40% to 45% of Taiwan's total stock market capitalization.

In a remarkable milestone, TSMC's weight in the MSCI Emerging Markets Index now exceeds India's entire country weighting. For global portfolio managers seeking AI exposure, buying Taiwan increasingly means buying TSMC.

South Korea: The Memory Chip Windfall

South Korea's ascent has been powered by two companies: Samsung Electronics and SK Hynix.

The AI boom has elevated both firms into the exclusive trillion-dollar valuation club. Together, they account for nearly half of South Korea's total market capitalization, transforming the country into one of the primary beneficiaries of exploding demand for AI memory and advanced semiconductor components.

The lesson is clear: ownership of critical AI infrastructure is attracting a disproportionate share of global capital.

The Capital Intensity Trap: Why India Lags in Hardware

To understand the performance gap, one must compare India's traditional IT services model with the semiconductor-driven economies of East Asia.

India's technology success has historically been built on labor arbitrage—delivering software development, maintenance, consulting, and outsourcing services at scale. While this model generated decades of growth, it lacks the proprietary technological moats and pricing power currently rewarded by investors.

The contrast is stark.

India's IT giants—including TCS, Infosys, and Wipro—collectively represent only about 8.48% of the Nifty 50. More importantly, they are viewed as service providers rather than owners of foundational AI technology.

Meanwhile, semiconductor leaders control intellectual property, manufacturing capacity, and supply chains that are virtually impossible to replicate quickly.

Building a modern fabrication facility requires tens of billions of dollars in capital expenditure, along with sophisticated ecosystems involving chemicals, industrial gases, power infrastructure, and highly specialized engineering talent. Despite progress through production-linked incentive (PLI) schemes, India remains years behind established semiconductor hubs.

"India slips to seventh in global market cap rankings as South Korea pulls ahead. It's time we stop equating service-based exports with the industrial hardware dominance of East Asia." — r/StockMarketIndia

AI-FOMO and the Flight of Global Capital

The AI boom has also triggered a massive reallocation of international investment.

Foreign Portfolio Investors (FPIs) pulled approximately $27.2 billion from Indian equities, pushing cumulative net foreign equity investments to their lowest levels since 2016.

The reason is straightforward: investors seeking immediate AI exposure found better opportunities in markets dominated by semiconductor manufacturers rather than software services providers.

This has fueled growing AI-FOMO among Indian investors. While the Nifty remains anchored by banks, financial services, and consumer companies that offer long-term stability, these sectors lack the explosive valuation expansion currently seen in AI-linked hardware businesses.

Macroeconomic Headwinds Amplified the Pressure

The AI narrative alone does not explain India's underperformance.

The domestic market has also faced a series of external shocks.

The Energy Risk

Escalating geopolitical tensions in West Asia and concerns surrounding disruptions to the Strait of Hormuz pushed Brent crude prices above $100 per barrel.

For an economy heavily dependent on imported energy, rising oil prices directly impact inflation, the current account deficit, corporate profitability, and investor sentiment.

The Monsoon Uncertainty

Further pressure emerged after forecasts suggested monsoon rainfall could reach only 90% of the long-term average.

For India, monsoon performance remains a critical economic variable. Weak rainfall can affect agricultural output, rural consumption, food inflation, and ultimately corporate earnings expectations.

Together, these factors created an environment where global investors had little incentive to remain overweight India when AI-driven alternatives were delivering significantly stronger returns.

Beyond the Ranking: The Bigger Economic Picture

Despite the stock market setback, India's broader economic position remains fundamentally different from South Korea's or Taiwan's.

India's GDP, estimated at roughly $4.15 trillion, remains more than double the size of South Korea's economy. The country continues to benefit from a growing middle class, rising consumption, expanding digital infrastructure, and favorable demographic trends.

The recent ranking drop therefore should not be interpreted as a decline in India's economic relevance.

Instead, it serves as a mathematical indicator of where global capital currently wants exposure.

The Bottom Line

India's fall to seventh place is not a verdict on the country's long-term prospects. It is a reflection of a global market increasingly obsessed with AI infrastructure, semiconductor manufacturing, and hardware ownership.

Taiwan and South Korea have become the primary beneficiaries of that trade because they control the factories, memory chips, and fabrication capacity powering the AI revolution.

India, by contrast, remains heavily exposed to financial services, consumption, and IT outsourcing—businesses that generate stable earnings but currently lack the valuation premium awarded to AI hardware leaders.

The warning for policymakers is clear: if India wants to compete for global capital at the highest levels during the next decade, it must move beyond being the world's back office and become a meaningful participant in the hardware ecosystem underpinning artificial intelligence.