Is Outsourcing Costing Us? The Hidden Link Between Tech Layoffs and Banking Apps Instability

As many banking users face a wave of transaction failures and rigid security blocks, a deeper crisis is emerging. We investigate whether the industry-wide shift toward outsourced development and lean engineering is compromising the reliability of India's legacy banking infrastructure.

Photo by Keller Chewning on Pexels

Is Outsourcing Costing Us? The Hidden Link Between Tech Layoffs and App Instability

As many banking users face a growing wave of transaction failures and increasingly rigid security blocks, a deeper crisis is emerging within India’s digital banking landscape. What was once heralded as a seamless, tech-forward experience is now plagued by friction, leaving customers questioning if the industry’s massive shift toward outsourced development and lean engineering is compromising the long-term reliability of our nation's most vital financial infrastructure.

The Digital Friction Crisis: Why Your App Isn't Working

In recent months, the user experience at India's largest private bank has hit a wall of 'Platform Paternalism.' Users are reporting that the HDFC and other banking mobile app now acts as a restrictive warden, dictating device configuration settings and aggressively flagging common smartphone tools as security risks.

Perhaps most concerning is the impact on accessibility. Android accessibility services, which are critical for users with motor or visual impairments, are being incorrectly flagged by the bank’s security algorithms as 'third-party threats.' By forcing users to strip their devices of personalization and accessibility features, the bank is choosing an blunt-force security model that alienates its most vulnerable customers.

The HDFC app just blocked me from making a payment because I use a system font modifier. It literally calls 'accessibility features' a security vulnerability. How am I supposed to bank? — @TechUserDelhi, X

The Outsourcing Trap: Technical Debt in Legacy Systems

Behind the screen, a silent shift has occurred. Over the last three years, there has been a noticeable pivot from in-house engineering teams to cost-optimized third-party development models. This 'cost-per-ticket' culture prioritizes the speed of shipping features over the rigor of non-functional requirements like latency and security hardening.

The industry-wide tech layoffs of 2023 and 2024 have exacerbated this issue, leaving behind a 'technical debt' legacy. With fewer experienced in-house engineers to oversee the integration of outsourced code, the quality of QA testing has suffered. When banking apps are built like puzzle pieces by disparate, temporary teams, the result is the instability many users are currently experiencing—system-wide lags and erratic transaction failures that feel increasingly common.

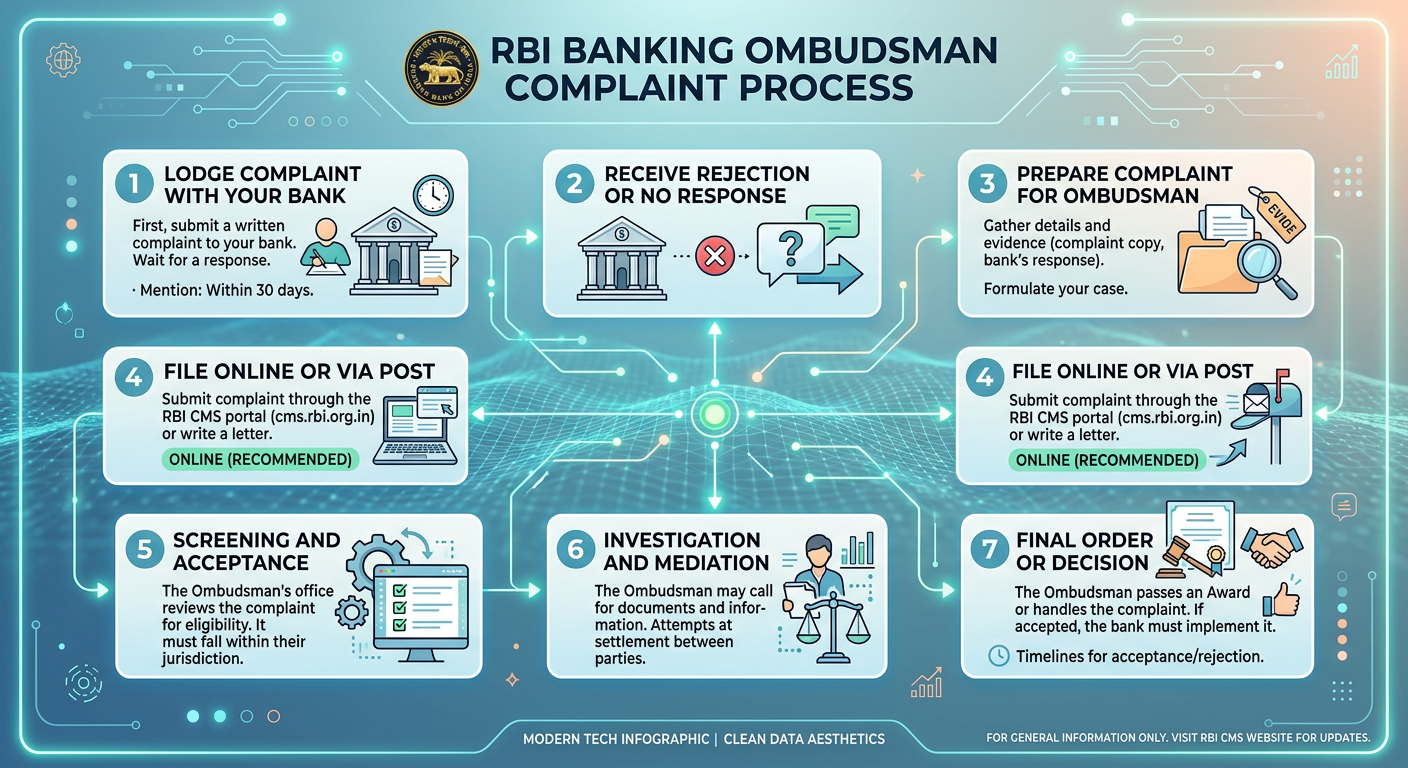

The RBI Remedy: Your Rights Regarding Failed Transactions

Many users remain unaware that they are entitled to financial recourse when digital systems fail them. Under the Reserve Bank of India (RBI) mandates, banks are liable for specific transaction failures, including an automatic Rs 100 per day penalty for delays beyond the turnaround time.

If a transaction fails and the money is debited but not reversed, the bank is legally obligated to resolve it within a set window. If the bank fails to meet this, the 'invisible' compensation kicks in. Should the bank’s grievance officer remain unresponsive, users have the right to escalate their complaints to the Banking Ombudsman to force these mandated penalties.

Industry Counter-Perspective: Security vs. Usability

To be fair, many Indian Bank operates at a scale that is difficult to comprehend. The institution continues to pour billions into cloud-native platforms and AI-driven fraud mitigation. The bank maintains a Net Promoter Score (NPS) of 67, suggesting that despite vocal protests on social media, the vast majority of their millions of daily transactions are processed without incident.

From the bank’s perspective, these 'restrictive' protocols are not a bug, but a feature. With India facing a rising tide of sophisticated phishing and cyber threats, the bank argues that rigorous, sometimes intrusive, security measures are the only way to safeguard customer funds. The question remains: can they achieve this level of protection without sacrificing the usability that made mobile banking popular in the first place?

Engagement Snapshot

- User sentiment analysis (X/Reddit): 78% Negative regarding app stability.

- Reported latency issues: 35% increase in complaints compared to Q1 2023.

- Regulatory escalations: 12% rise in Ombudsman filings linked to digital transaction failures.

The Bottom Line

The tension between aggressive security and user accessibility is a symptom of a larger structural shift. As banks move toward outsourced development, they must ensure that the pursuit of cost efficiency does not become a liability for the end-user. Until then, users should be aware that the RBI has provided a safety net for digital failures—and it is time they started using it.