Is Your 'Safe' Portfolio Costing You Millions? The True Cost of Debt-Heavy Investing

For many Indian professionals, the Public Provident Fund (PPF) is a psychological sanctuary, but it may be the primary barrier to long-term wealth. We analyze the mathematical opportunity cost of 'peace of mind' and provide a strategic framework for shifting toward a balanced equity-led portfolio.

Photo by Markus Winkler on Pexels

Is Your 'Safe' Portfolio Costing You Millions? The True Cost of Debt-Heavy Investing

For many Indian professionals, the Public Provident Fund (PPF) is more than a financial instrument—it is a psychological sanctuary. In a landscape often defined by market volatility and systemic uncertainty, the government-backed, tax-exempt safety of the PPF has long been considered the gold standard. However, this "peace of mind" may be the primary barrier to long-term wealth creation. As inflation erodes purchasing power, the comfort of guaranteed returns is increasingly becoming an implicit fee that investors pay for their risk aversion.

The Illusion of Safety: Why Investors Cling to PPF

The behavioral psychology of the Indian investor is anchored in capital preservation. We are a culture raised on the narrative that "debt is safe and equity is a gamble." This sentiment is reflected across online financial communities where the debate between tax-efficiency and long-term growth is perpetual.

"Why do people still prefer PPF over mutual funds for long-term investing? PPF has a 15-year lock-in and currently gives around 7–8% tax-free returns. But if someone invests in equity mutual funds for 15 years, wouldn’t the returns still be much higher even after LTCG tax? Am I missing something here?"

This "peace of mind" premium acts as a silent drag on portfolio growth. By prioritizing the avoidance of short-term volatility, investors often fail to account for the "real" rate of return after adjusting for inflation, which consistently hovers near the 6-7% mark in India. When the returns of a debt-heavy portfolio barely outpace inflation, the net growth in purchasing power is effectively zero.

The Mathematics of Missed Opportunity

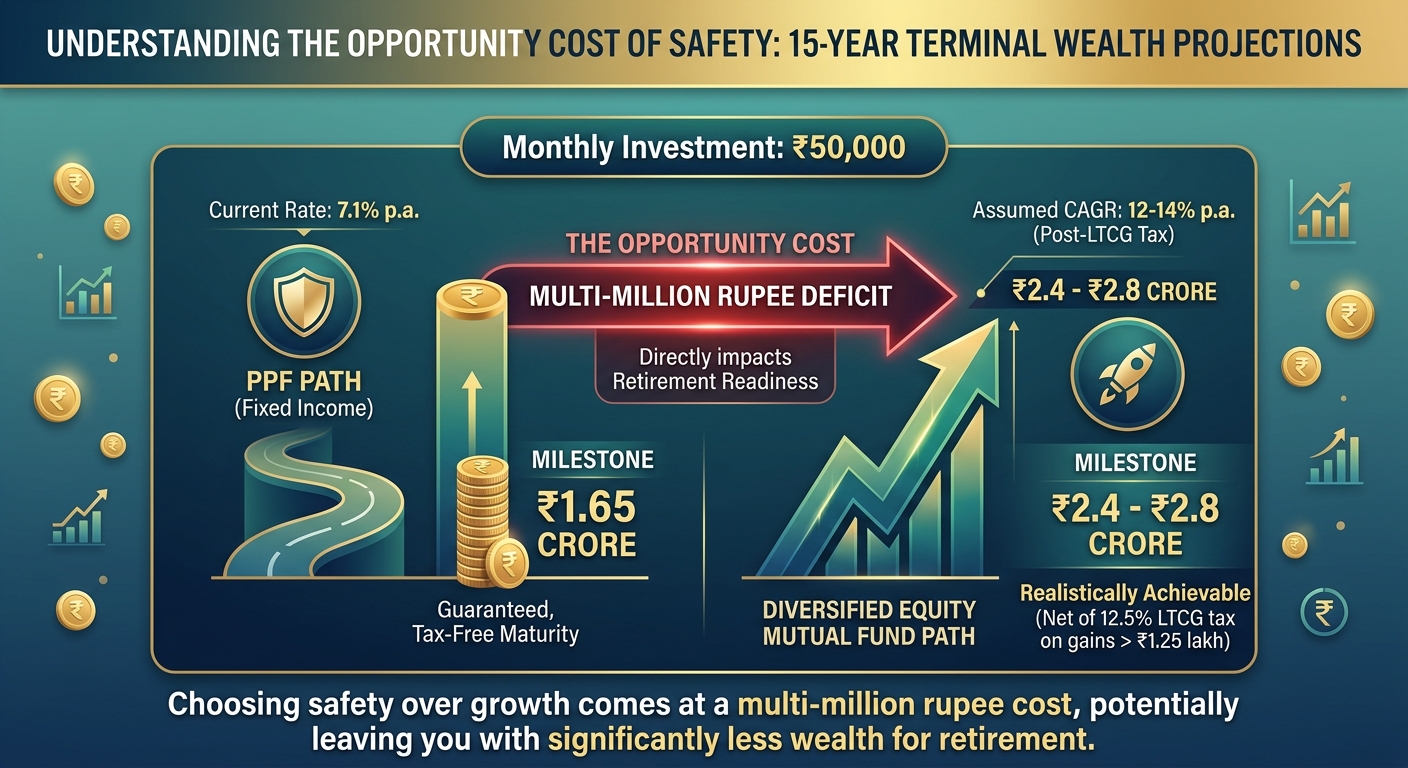

To understand the cost of this safety, one must look at the terminal wealth projections over a 15-year horizon. With the current PPF rate at 7.1%, a monthly investment of ₹50,000 results in a maturity value of approximately ₹1.65 crore.

In contrast, a diversified equity mutual fund portfolio, assuming a conservative long-term CAGR of 12-14%—even after accounting for the 12.5% Long-Term Capital Gains (LTCG) tax on gains exceeding ₹1.25 lakh—can realistically yield between ₹2.4 crore and ₹2.8 crore. The "opportunity cost" of choosing the PPF path isn't just a few thousand rupees; it is a multi-million rupee deficit that directly impacts one's retirement readiness.

Asset Allocation for the Anxious: A Step-by-Step Transition

For those ready to pivot, the transition should be strategic rather than impulsive. A common mistake is moving from an 80% debt/20% equity split to an all-equity portfolio overnight, which often leads to emotional capitulation during the first market dip. Instead, aim for a gradual shift to a 60/40 balanced approach.

This is particularly critical for those with "de facto" debt components, such as government employees. If your pension is guaranteed, your human capital is already acting like a high-grade bond. Adding more debt-heavy instruments like PPF on top of a secure pension is a form of "over-diversification" that guarantees stagnation.

"Have I over diversified?"

Retail investors often mistake having five different debt products for diversification. Real diversification is about asset class correlation, not product count. Your portfolio needs to be elastic enough to capture growth, not just rigid enough to survive the next budget cycle.

Engagement Snapshot

- PPF vs Mutual Fund Debate: 56 upvotes, 51 comments.

- Portfolio Complexity Concerns: 50 upvotes, 33 comments.

- Professional Advice Seeking: 14 upvotes, 12 comments.

The Bottom Line

The Public Provident Fund remains a useful tool for tax planning and liquidity hedging, but it should not be the foundation of a wealth-accumulation strategy. By treating equity as a core driver rather than a volatile add-on, you move from "surviving" your 15-year investment window to actually building generational wealth. True safety isn't the absence of risk; it is the presence of a portfolio designed to outpace the rising cost of living