Sentiment Over Strategy: Why Young Indians Are Prioritizing 'Emotional Assets'

A surge in young investors is forcing a rethink of modern portfolio theory as Gen Z balances ancestral legacies with digital-first financial growth. We explore why physical gold and sentimental assets are winning over aggressive market strategies for India's youngest wealth builders.

Photo by Ketut Subiyanto on Pexels

Sentiment Over Strategy: Why Young Indians Are Prioritizing 'Emotional Assets'

A surge in young investors is forcing a rethink of modern portfolio theory as Gen Z balances ancestral legacies with digital-first financial growth. We explore why physical gold and sentimental assets are winning over aggressive market strategies for India's youngest wealth builders.

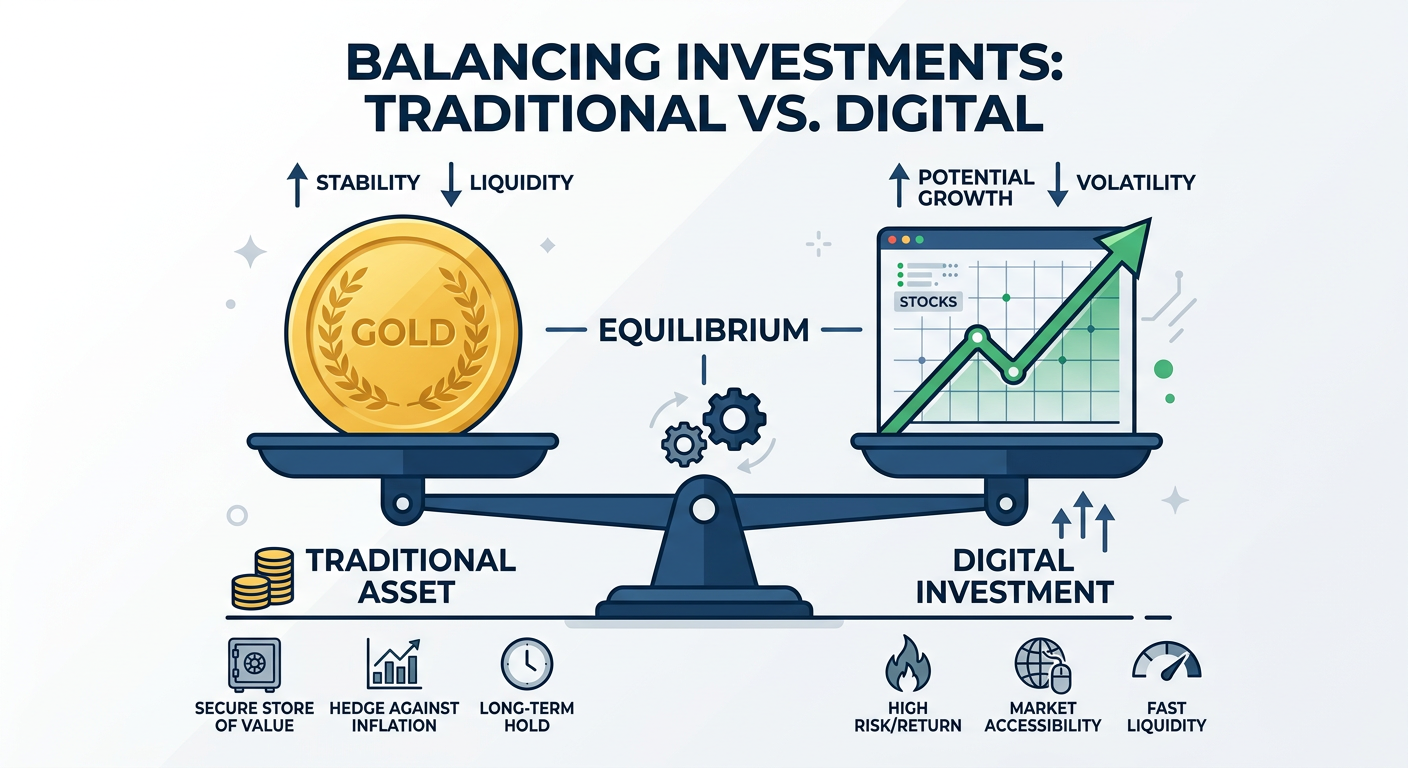

The Inheritance Dilemma: Legacy vs. Growth

For many 19-to-21-year-old Indians, the journey into finance doesn't begin with a whitepaper on equity markets, but with a small, emotionally charged inheritance. Whether it is a sum of ₹16,000 left by a grandfather or a stash of gold coins passed down through generations, these assets represent a bridge between traditional safety nets and modern aspirations.

In the digital age, financial advice often focuses on the cold mathematics of CAGR and portfolio diversification. However, for a student living on a tight budget—often ₹2,500 per month—the "wealth maximization" narrative feels disconnected from their reality. These young investors aren't just managing currency; they are managing the psychological safety of an emotional keepsake.

"grandfather left 16k for me, i haven't spent a rupee yet and i do not know what to do with it, PLEASE HELP. I come from a middle-class family... he was more like a father to me, so this money means a lot emotionally as well." — u/anonymous_student, r/IndiaInvestments

The ROI of Sentiment: Gold and Generational Values

There is a deep-seated intergenerational tension at play. While fintech platforms preach the liquidity of Gold ETFs and the efficiency of index funds, many young Indians feel a powerful "path dependency" toward physical assets. Parental influence often reinforces gold not as a financial hedge, but as a cultural identity marker.

For Gen Z, physical gold functions as an "emotional store of value." It is an asset they can hold, display, and associate with their lineage. While seasoned advisors might label this as an "inefficient" investment due to making charges and storage risks, the community consensus often leans toward preservation over optimization.

""Buy 1 gram of gold and keep it as his remembrance. Sell it only when you are in dire need of money. Until then, it stays with you." — u/community_mentor, r/IndiaInvestments

Financial Literacy for the ₹2,500 Budget

The standard financial advice often cited in Western literature—such as building a 6-month emergency fund—is frequently irrelevant to the Indian student experience. When your entire monthly budget is ₹2,500, saving for a liquid emergency fund can feel like an impossible hurdle that prevents actual wealth creation.

Instead, the new wave of young investors is turning to fractional investing. With low-cost fintech apps that simplify the KYC process and allow for SIPs (Systematic Investment Plans) starting as low as ₹100, the entry barrier has been demolished. The shift here is from "saving to spend" to "investing to participate." By choosing index funds over stock picking, these students are learning that consistency often beats technical prowess.

Beyond the Stock Market: Skill-Based Investing

Perhaps the most overlooked asset class for a 20-year-old is the "Human Capital" account. When managing a small corpus, the opportunity cost of locking money in a brokerage account versus spending it on a professional certification can be vast.

We are seeing a "Digital Native Advantage" where students leverage these fintech tools not just to accumulate wealth, but to understand the mechanics of the economy. The real gain at this stage isn't the 8-12% annual return—it is the financial literacy gained by navigating tax liabilities and market cycles early. Balancing the preservation of the "ancestral gold" with the growth of a "digital SIP" creates a hybrid portfolio that respects the past while betting on the future.

Engagement Snapshot

- Primary Demographic: 19-22 years old

- Average Starting Capital: ₹10,000 - ₹25,000

- Preferred Platforms: Low-cost, UI-first discount brokers

- Community Sentiment: High trust in peer-to-peer mentorship; skeptical of "get rich quick" influencer content.

The Bottom Line

For India’s youngest investors, the portfolio is not just a ledger of returns—it is a reflection of identity. While financial experts might demand they dump their physical gold into high-yield instruments, the reality is that "emotional assets" provide the stability necessary to stay in the game for the long haul. The smartest way to invest at 20 isn't just about the numbers; it's about building a financial habit that aligns with your values.