Should You Force Your Kids to Invest? The Hidden Costs of the 10% SIP Rule

As Indian parents increasingly push the 10% Systematic Investment Plan (SIP) rule on young earners, a debate brews: is this financial empowerment, or is it transferring intergenerational anxiety? We explore the thin line between disciplined wealth creation and the psychological burnout threatening India's next generation.

Photo by Ravi Roshan on Pexels

Should You Force Your Kids to Invest? The Hidden Costs of the 10% SIP Rule

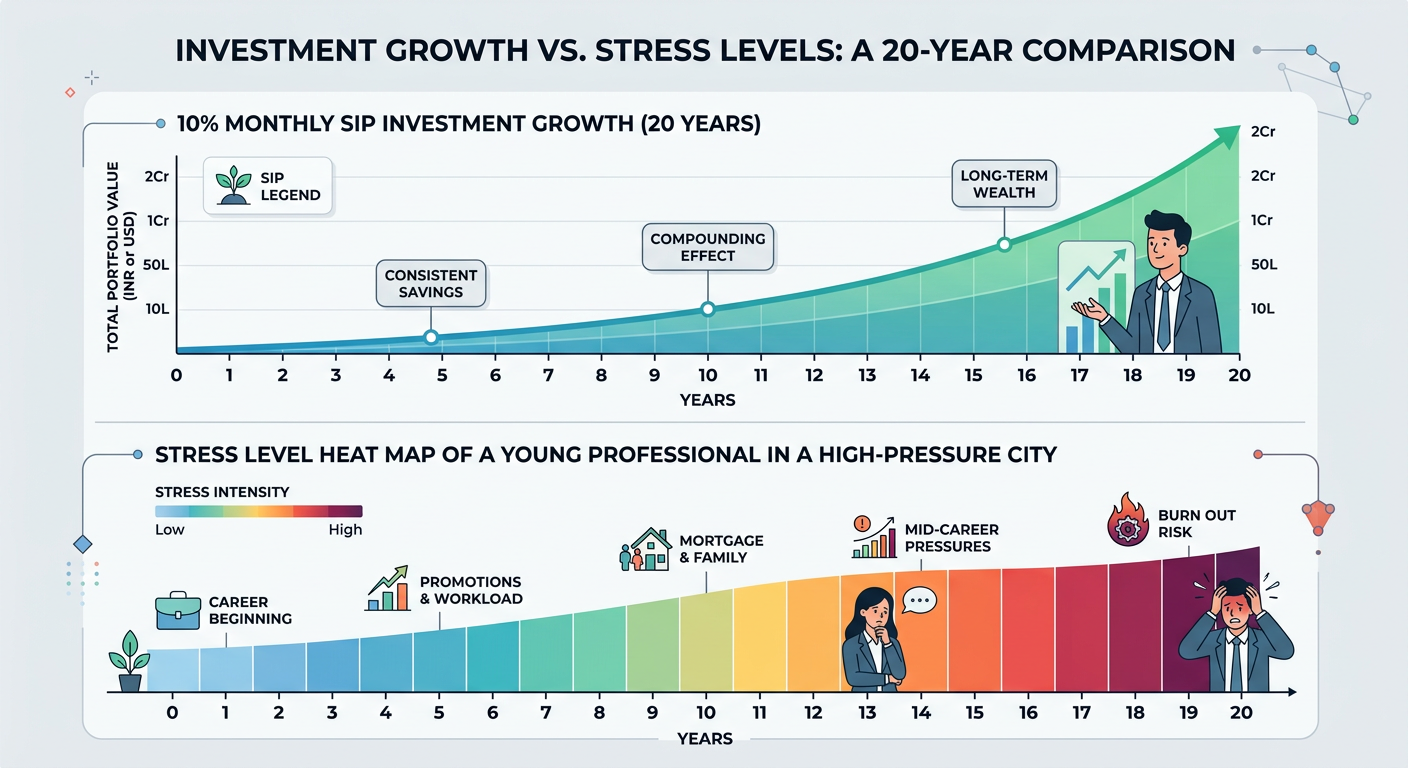

As the first paychecks hit the bank accounts of India’s Gen Z workforce, a familiar scene unfolds at the dining table. It is no longer just about career advice; it is about the "10% SIP Rule." Parents, fueled by the memory of missing out on the early equity boom, are increasingly mandating that 10% to 20% of a child’s starting salary be funneled into systematic investment plans (SIPs). While the intent is undeniably rooted in securing a stable future, a growing concern is emerging: are we empowering our children, or are we simply transferring intergenerational financial anxiety onto them?

The Rise of the 10% Mandate

Historically, the Indian middle class relied on the safety of the Public Provident Fund (PPF) and gold. Today, the conversation has shifted toward aggressive wealth creation. The narrative is clear: beat inflation through early compounding. However, this has transformed the first paycheck—once a symbol of personal achievement and independence—into a stress-inducing administrative burden.

By viewing income strictly as an investment vehicle, young professionals often feel a sense of 'guilt-spending.' When every rupee is earmarked for a portfolio, the room for self-discovery, travel, or even the occasional impulse purchase disappears. This rigid approach prioritizes future wealth at the cost of present-day autonomy.

The Math of Compounding vs. The Cost of Burnout

From a purely mathematical standpoint, starting at age 22 is an incredible advantage. With an assumed 12% annual return, a modest monthly investment of ₹10,000 could balloon to over ₹3.5 crore in 30 years. Yet, the cost of this discipline is often paid in mental health.

We are witnessing a generation caught between the pressure to "FIRE" (Financial Independence, Retire Early) and the reality of a demanding, high-attrition corporate environment. When the expectation to save is decoupled from the freedom to enjoy, the resulting burnout leads to early career dissatisfaction.

"Agriculture contributes around 16% of India’s GDP while employing around 45% of the country’s workforce. Many people remain in agriculture because they have limited alternative options. Unless we create more non farm and manufacturing jobs, it will be very difficult to sustainably increase our GD" — @dmuthuk, X

Policy as a Safety Net: Decoding EPFO 3.0

For many young earners, the rigidity of traditional tax-saving instruments often led to panic-driven liquidity crises. However, the landscape is changing. There have been recent shifts in EPFO regulations in India, moving toward an 'Eligible Member Balance' system.

This shift is transformative. It moves away from strict 'reason-based' withdrawals—which required proving a house purchase or a medical emergency—toward a more flexible, state-sanctioned sabbatical fund. For the modern employee, this functions as a critical safety net, allowing them to take professional risks or breaks without liquidating their long-term equity SIPs, effectively bridging the gap between rigid saving and modern life liquidity.

Navigating Disparity: Finances for Couples

When two young professionals marry, income disparity often creates a 'power struggle.' However, savvy couples are rebranding this as a 'resource allocation' strategy. Instead of insisting that both partners contribute equally to high-pressure investments, they focus on transparent communication.

This is particularly vital given the 'hidden tax' of social media-driven wedding debt, which can derail a couple’s finances before they even begin. Rather than rigid individual rules, the healthiest dynamic is one where the 'provider' mindset is replaced by a partnership model, ensuring that one partner’s financial growth does not come at the expense of the other’s mental well-being.

The Bottom Line

Financial literacy should not be confused with financial control. If the 10% SIP rule feels more like a shackle than a strategy, it is time to pivot the conversation. True wealth is built not just through compounding interest, but through the ability to make choices that align with one's long-term mental health. Parents should act as mentors who explain the power of the market, not as auditors who audit every pay stub. After all, the goal of wealth is to buy freedom, not to trade it for a future that feels like an obligation.