Stop Collecting Mutual Funds: How 'Diworsification' is Quietly Killing Your Returns

Indian retail investors are increasingly trapped in the 'diworsification' cycle, holding dozens of funds that dilute returns and complicate wealth management. This guide explores why pruning your portfolio to 4-6 funds can optimize performance and reduce cognitive overload.

Stop Collecting Mutual Funds: How 'Diworsification' is Quietly Killing Your Returns

The democratization of finance via slick, mobile-first investment platforms has been a double-edged sword. While access to the equity markets is at an all-time high, the 'infinite shelf' of available mutual funds has triggered a widespread case of decision paralysis among young retail investors between 23 and 35 years old.

In a frantic attempt to capture every hot sector, trending theme, or new launch, investors accumulate collection folders of mutual fund schemes. They run multiple active funds concurrently, operating under the dangerous psychological illusion that more fund names on a dashboard equals more safety.

But when structural market shocks hit home, the harsh reality of this strategy is completely exposed. During a sudden final-hour selloff today on Friday, May 29, 2026, the benchmark NSE Nifty 50 plummeted 359.40 points (1.50%) to close at 23,547.75, while the BSE Sensex plunged 1,092.06 points. Everyday investors opened their apps expecting their sprawling setups to cushion the blow, only to watch every single active scheme sink in absolute unison.

This phenomenon is known as 'diworsification'—the tipping point where adding more funds creates so much structural overlap that you no longer achieve true risk mitigation. Instead, you simply recreate a high-cost, cluttered version of a broad market index fund while paying premium active management fees. The cognitive load of tracking dozens of automated transactions often leads to complete abandonment, where investors lose sight of long-term goals amid the noise of daily market volatility.

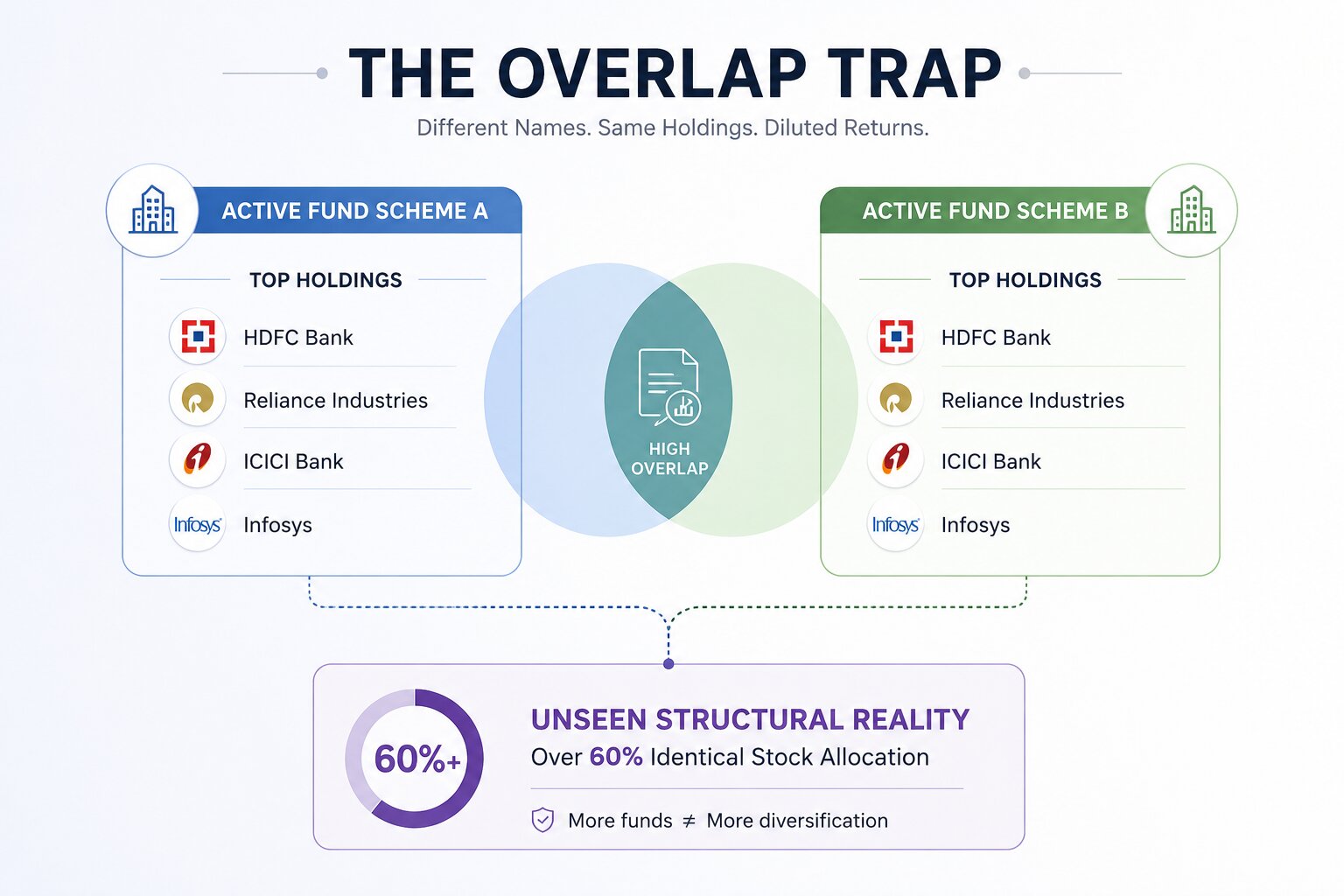

The Portfolio Overlap Illusion: Breaking Down the Clutter

Statistically, a retail portfolio captures broad market beta and hits structural saturation with as few as 4 to 6 funds. Anything beyond that introduces severe redundancy. Mutual fund categories are mere regulatory mandates; they do not bar separate asset managers from chasing the exact same high-liquidity corporations.

When you use portfolio X-Ray tools to analyze your holdings, you will often find that your different diversified schemes share over 60% of the same underlying stocks. Because the largest, most liquid blue-chip companies dominate institutional holdings, different active fund types heavily clone each other's core stock-level architectures.

By holding both categories, you are merely compounding the expense ratio drag without gaining any real risk-adjusted advantage. Every extra overlapping fund simply dilutes your winners, doubles your management fees, and creates a massive drag on final wealth generation.

Live Comparison: Active Duplication vs. The Lean Portfolio Strategy

| Structural Portfolio Metric | The Over-Diversified Basket (10+ Funds) | The Lean Portfolio Strategy (4-6 Funds) |

|---|---|---|

| Typical Fund Count | 8 to 15 active mutual fund schemes. | Max 4 to 6 highly distinct funds. |

| Total Underlying Stocks | 150+ unique companies (Massive unseen clutter). | 45 to 65 highly targeted corporate positions. |

| Average Portfolio Overlap | High. Frequently scales over 60% across schemes. | Minimal. Maintained under 15% stock-level overlap. |

| Expense Load Impact | High. Multiple active fees dragging down net compounding. | Optimized. Drastically lowers cumulative fee percentages. |

| Tracking Complexity | High. Complex tax-harvesting tracking across 5+ AMCs. | Clean and simple. Takes 5 minutes to audit once a quarter. |

| Alpha Generation Capability | Diluted. The winners are too small to impact your real wealth. | Concentrated conviction allows true outperformance to scale. |

De-cluttering Without the Financial Hangover

Pruning a portfolio is not just an aesthetic exercise; it is a clinical one. Before hitting the 'Redeem' button, remember that exiting mutual fund investments can trigger tax liabilities, including Exit Load and Capital Gains tax. When exiting equity mutual funds in India, any units sold within 1 year of allocation face an Exit Load (typically 1%) along with Short-Term Capital Gains tax. If your units have crossed the 365-day threshold, they qualify for Long-Term Capital Gains (LTCG) tax.

- Audit for Overlap: Use tools like Kuvera or Value Research to check common stock holdings across your AMCs. Identify which funds share more than 30% of the same stock architecture.

- The 3-Year Threshold: If a fund is performing poorly but is nearing its exit load period (usually 1 year), wait. It is rarely worth paying a 1% exit load to shift money that can stay put while you stop fresh inputs.

- Stop, Don't Sell: Instead of liquidating everything immediately, stop the automatic inputs in redundant funds first. This redirects cash flow to your highest conviction lines without triggering immediate tax events, letting old units age out until they clear their exit penalty windows entirely.

Beyond the Platform: Rationalizing Financial Decisions

We are currently seeing a wide gap between the ease of 'one-tap' investing on sleek applications and sound financial literacy. Is 'under-diversification' a rational response? Perhaps. By limiting choices, investors force themselves to actually research their conviction, rather than picking the top 10 funds in a search results list.

Future-proofing your portfolio requires shifting from a 'product-first' mindset to a 'goal-first' framework. Whether you are saving for long-term independence or a house down payment, a portfolio should be built to meet a targeted timeline, not to capture a temporary market trend. If your portfolio requires a complex tracker spreadsheet to monitor, it is already too complex.

Engagement Snapshot

- Sentiment Trend: Investors are increasingly vocal about 'Fintech fatigue,' with 65% of community sentiment in financial threads skewing toward 'simplification' over 'feature-rich' dashboards.

- Search Growth: Interest in 'Portfolio Consolidation' and 'Mutual Fund X-Ray' has surged by 40% year-on-year among urban Indian retail investors.

The Bottom Line

In the world of investing, less is often significantly more. By limiting yourself to a tight, focused allocation, you reduce the 'diworsification' trap, lower your cumulative expense ratios, and regain your financial sanity. Audit your holdings, stop the overlap, and focus on the clean power of compounding rather than the clutter of collection.