Stop Fund-Hopping: Why Your SIP Performance Anxiety Might Be Costing You Crores

Young professionals are increasingly ditching their mutual funds at the first sign of volatility, treating portfolios like day-trading accounts. We break down the math behind the 'fund-hopping' trap and offer a definitive decision framework to stay the course toward your first crore.

Photo by Tima Miroshnichenko on Pexels

Stop Fund-Hopping: Why Your SIP Performance Anxiety Might Be Costing You Crores

For the young professional in Bengaluru, the goal is often simple: hit that first crore as quickly as possible. But between the astronomical rent deposits in HSR Layout, the lure of 'get-rich-quick' trading apps, and the constant pings of underperforming SIPs, the path to wealth has become a high-stakes obstacle course. Far too many investors are falling into the 'fund-hopping' trap, treating their long-term portfolios like day-trading accounts, only to find their compounding returns shredded by taxes and exit loads.

The Bangalore Syndrome: Lifestyle Inflation and the 'Crore' Myth

New entrants to the workforce often face the 'Relocation Trap'. The upfront costs of moving to a Tier-1 city—security deposits, brokerage fees, and furnishing—can cannibalize up to 30-40% of a year’s potential seed capital. This initial liquidity crunch often forces young professionals to delay their SIP journey, making every subsequent rupee work harder.

While the 50-30-20 rule is a standard financial framework often modified for metro living expenses, the reality of urban inflation requires aggressive recalibration. Many young investors fall into the 'Psychological Safety Trap', opting for Recurring Deposits (RDs) instead of equities because they fear the red color on their portfolio dashboard. While RDs feel 'safe', they often fail to beat post-tax inflation, effectively losing purchasing power over a 10-year horizon.

"#MCPersonalFinance | Picking the right mutual fund can matter more than picking the right category. Choosing the right mutual fund can be just as important as picking the right category. Here's why fund selection deserves a closer look. By @PriyadarshiniM9 : https://t.co/lm4wpThup0" — @moneycontrolcom

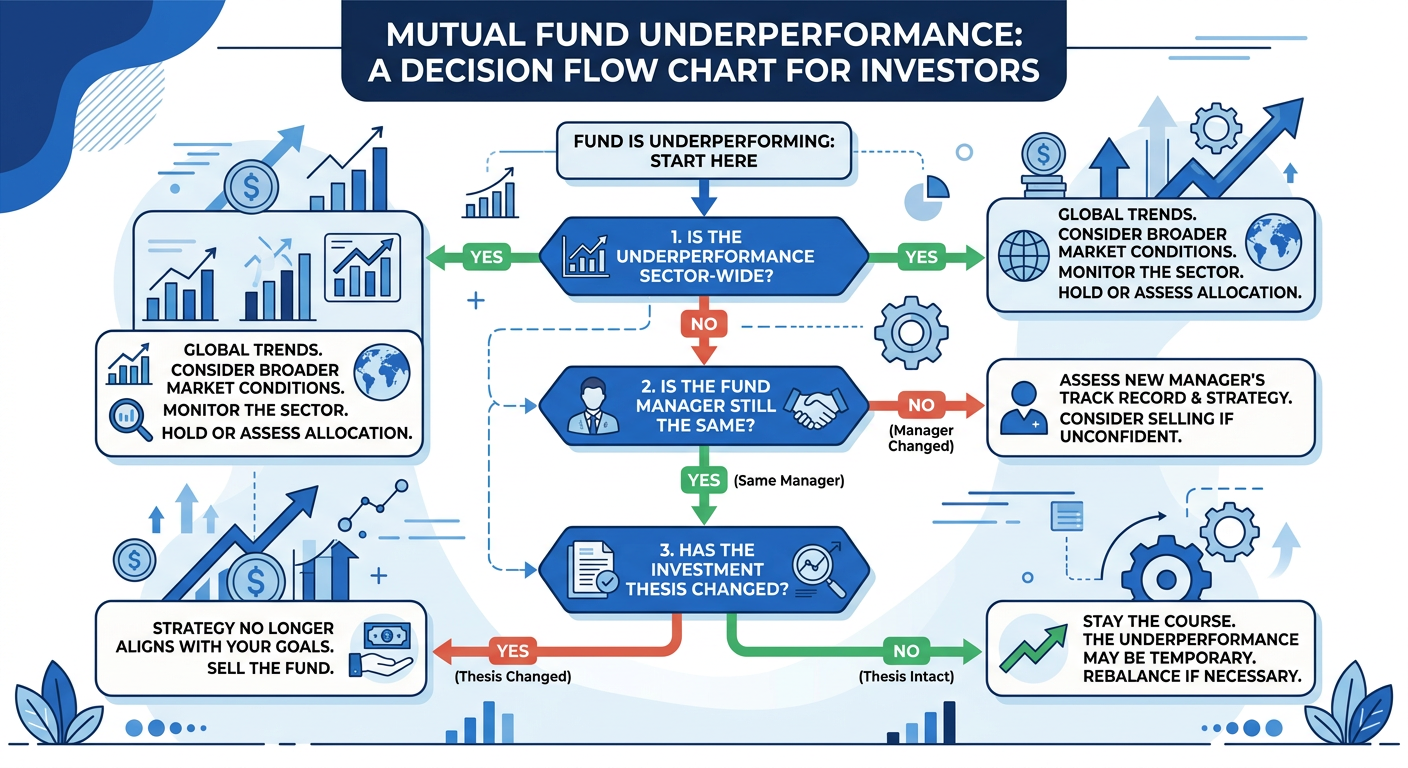

The Fund-Hopping Fallacy: When Market Cycles Get Misread as Underperformance

When a large-cap fund dips by 5%, panic-selling it to 'chase' a trending mid-cap fund is rarely a tactical genius move; it is usually a tax-inefficient mistake. Each time you switch funds, you trigger capital gains taxes and reset your compounding clock.

""#LeadStoryOnET | Should you switch your mutual funds after a few months? Expert offers a reality check https://t.co/5DfF6pFr8f" — @EconomicTimes

Investors must distinguish between a 'market cycle trough'—where the entire sector is down—and 'systemic management failure'. If your fund is trailing its benchmark consistently over 3 to 5 years, that is a red flag. If it is trailing for two quarters during a broad market correction, that is noise.

A Decision Framework for Your Portfolio

To move from anxiety-driven hopping to a structured wealth-building machine, follow this logic:

- Quantitative Red Flags: Is the tracking error significantly higher than the peer group average? Has there been a consistent change in the fund manager followed by a shift in investment style? If yes, evaluate a move.

- The Debt-to-Equity Transition: For those stuck in RDs, shift to a 'Liquid Fund' or 'Arbitrage Fund' as an intermediate step to lower the tax impact, then gradually ladder your entries into index or flexi-cap equity funds.

- Inflation-Adjusted Goals: Don't aim for a static crore. With 6-7% average inflation, your target for a comfortable life in a city like Bengaluru needs to be pegged at 1.5x to 2x your current valuation estimate to account for purchasing power parity over the next decade.

The Bottom Line

Wealth creation is a marathon run at a sprinter's pace. If you are constantly hopping funds, you aren't building a portfolio—you are paying the brokerage and the taxman to play a game you cannot win. Pick a solid, low-cost index or a proven multi-cap fund, automate your SIP, and stop checking your app daily. Your future self—and your tax liability—will thank you.