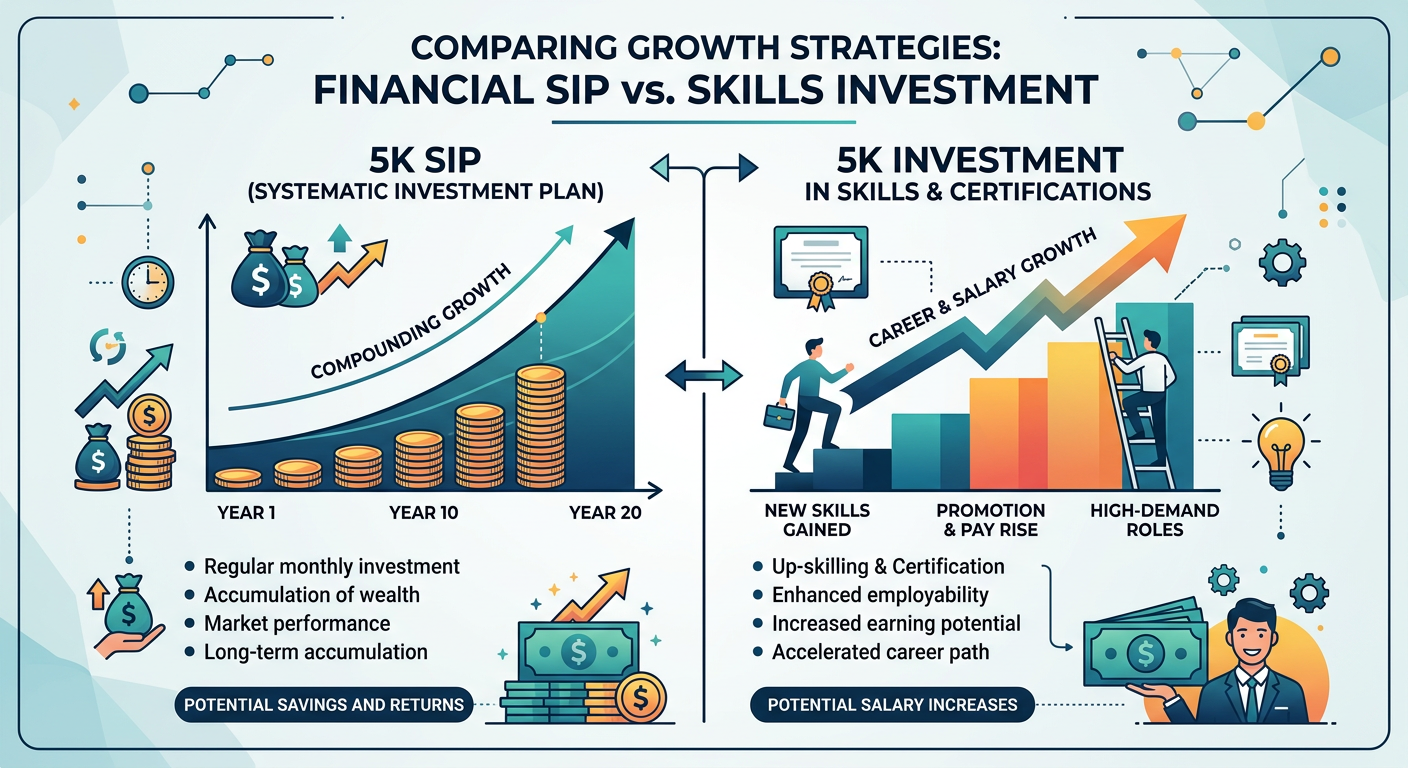

Stop Obsessing Over the 1 Crore Mark: The ROI of Upskilling vs. Investing

Gen Z is chasing the '1 Crore by 30' goal through aggressive SIPs and portfolio optimization, often at the cost of their primary asset: their earning potential. We analyze why professional upskilling often yields higher long-term returns than squeezing every rupee into equity early in your career.

Photo by AlphaTradeZone on Pexels

Stop Obsessing Over the 1 Crore Mark: The ROI of Upskilling vs. Investing

Gen Z is chasing the '1 Crore by 30' goal through aggressive Systematic Investment Plans (SIPs) and rigorous portfolio optimization. While the math behind the power of compounding is indisputable—starting at 20 versus 25 results in a massive delta in terminal wealth—there is a growing disconnect in the advice being dispensed. We are pushing young professionals to hoard capital at the very moment they should be deploying it into their most potent asset: their earning potential.

The 1 Crore Myth and the Math of Early Career Austerity

For a 23-year-old making a starting salary, the psychological burden of a 7-figure milestone can lead to 'austerity trap.' While current financial advice for young investors often suggests SIPs as a wealth creation strategy, there is a diminishing return on extreme frugality. If you are saving 50% of a modest income, you are effectively capping your ability to network, travel for industry events, or invest in certifications that could double your salary in three years.

"I see so many peers stressing over their 20k SIP while working a job that barely pays for their commute. They have the math of a pensioner but the income of a trainee. — @FinTechRahul, X

The mathematical reality is that your salary growth curve in your 20s acts as a much higher multiplier than any Nifty 50 index fund can provide. A 20% jump in your annual base salary, achieved through professional upskilling, far outweighs the returns of a few thousand rupees invested in equity during the early, low-capital years of your career.

The ROI of You: Why Upskilling Trumps Aggressive Allocation

Think of your current salary as 'startup capital.' Just as a VC-backed firm wouldn't dump all its cash into a passive high-yield account instead of product development, you shouldn't dump all your liquidity into market funds if your 'product'—your skill set—is stagnant.

Professional upskilling has an Internal Rate of Return (IRR) that is often significantly higher than the standard 12-15% equity market return. When you invest in a niche certification, a high-end conference, or a specialized executive program, you are buying a permanent increase in your 'human capital dividend.' Once you reach a higher income bracket, your ability to sustain a larger SIP becomes frictionless, rather than a monthly battle against your bank balance.

The Sandwich Generation Trap and Lifestyle Creep

Indian professionals face a unique challenge: the 'Sandwich Generation' trap. Many are balancing personal wealth goals with increasing familial responsibilities. This is compounded by 'subscription-based living'—the invisible drain of OTT, SaaS, and gig-economy services that turn minor costs into major liquidity leaks.

Instead of static SIPs that cause stress during market corrections, consider 'escalating SIPs.' Tie your investment increases to your salary hikes rather than a fixed commitment. This allows for a lifestyle buffer and ensures you aren't forced to exit your positions during a bear market just to cover basic living expenses—the dreaded 'behavioral gap' that haunts retail investors.

Practical Strategies: Scaling for Volatility and Tax

When it comes to portfolio hygiene, simplicity is your best defense against volatility.

- Liquidity vs. Yield: For emergency funds, debate continues between traditional RDs and Debt Mutual Funds. While Debt Funds offer better tax efficiency for those in higher tax brackets, RDs provide the psychological safety of principal protection.

- Tax-Efficient Rebalancing: Use the 1.25 lakh LTCG exemption on equity shares and equity-oriented units to your advantage. Rebalance annually to prune underperformers without triggering unnecessary tax liabilities.

- Behavioral Safety: Automate your investments to bypass emotional decision-making. If the market dips, your automated instruction keeps buying, effectively lowering your cost basis without you having to stare at the red screen.

The Bottom Line

Don't let the '1 Crore by 30' narrative blind you to the reality of the compounding power of your own career. Your early 20s are not for maximizing your tax-free dividends; they are for maximizing your professional throughput. Invest in your skills, scale your income, and let the market compounding take over once you have the capital base to make the math truly work for you.