Structural Fragility: Why India’s Oil Dependency Remains the Rupee’s Biggest Achilles' Heel

As the rupee hits the psychological 96 mark against the dollar, the shadow of 100 looms over Indian households. We analyze why India's persistent energy import dependency is keeping the currency under pressure and whether current transition policies offer a realistic escape.

Photo by Ravi Roshan on Pexels

Structural Fragility: Why India’s Oil Dependency Remains the Rupee’s Biggest Achilles' Heel

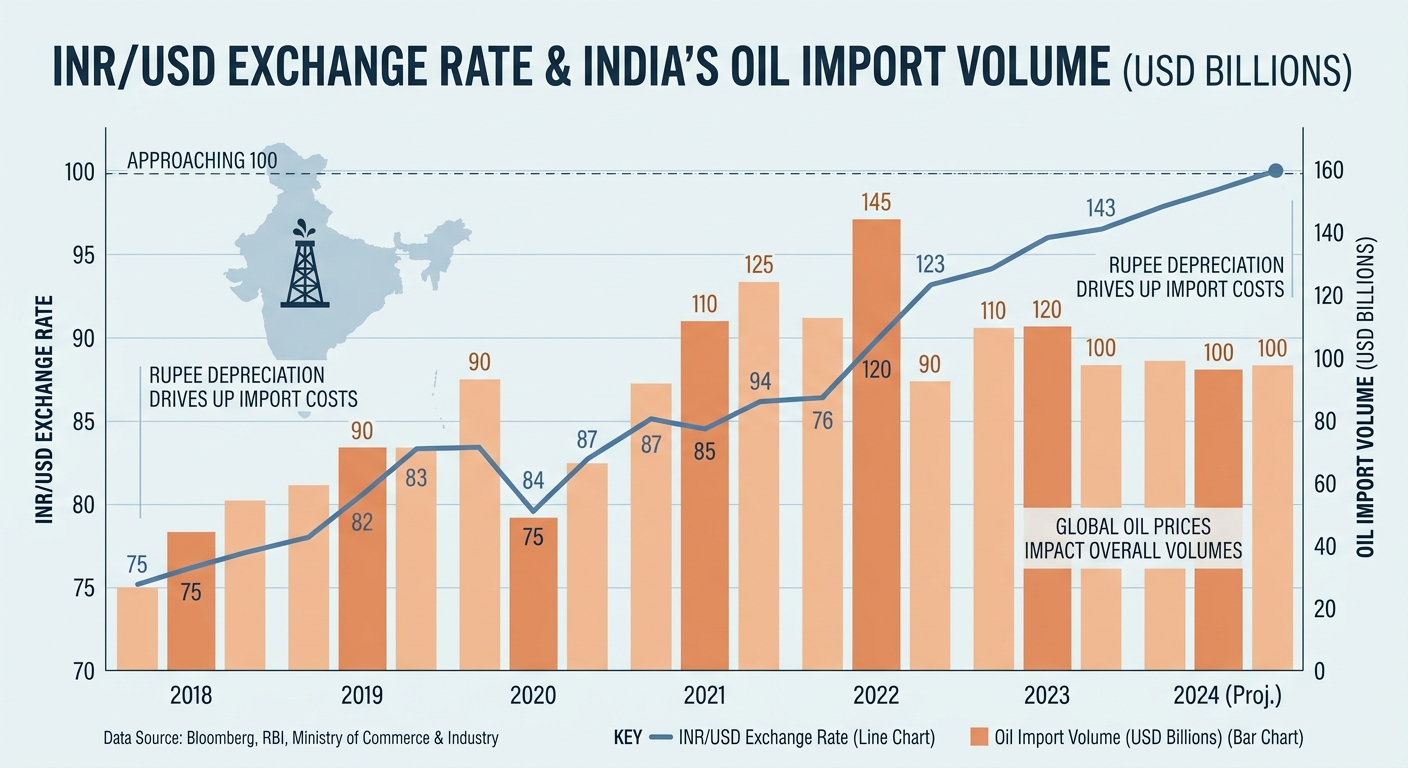

As the Indian Rupee (INR) breaches the psychological 96-mark against the US Dollar, the conversation on Indian social media has shifted from technical market analysis to genuine, widespread anxiety. The shadow of the 100-rupee barrier no longer feels like a distant theoretical possibility, but an imminent reality. While global factors—such as the strengthening greenback and persistent FII outflows—are the usual culprits, the core of India’s currency trouble remains anchored in a structural reality: an insatiable, import-heavy energy appetite.

The 96 Breach: Beyond the Psychological Barrier

For the common Indian investor, the transition from a 'strong dollar' narrative to one of 'structural weakness' is becoming increasingly apparent. The breach of 96 is more than just a number; it is a signal that the protective layers of forex reserves and central bank intervention are struggling to mask a deeper underlying instability.

"I was just casually checking the INR conversions to other currencies and realised INR has devalued at around 12-14% in the past one year. Why is no one talking about this? As a normal man, its hard to understand what is the reason behind this."

— u/retail_trader, r/indianeconomy

This sentiment reflects the growing disconnect between official macroeconomic optimism and the lived experience of inflation. When the rupee weakens, it is not just stocks that jitter; the cost of living—from imported electronics to edible oils—begins a slow, grinding ascent that hits middle-class wallets long before it appears in official CPI data.

The Oil Nexus: Why Every Dollar Matters

India’s status as a top-tier energy importer remains the single greatest drag on its currency. With the country importing roughly 85% of its crude oil, every marginal increase in global oil prices acts as a direct tax on the Rupee. Despite aggressive policy pushes for Electric Vehicles (EVs) and massive investments in renewable energy, the transition is essentially a slow-motion process compared to the immediate, high-velocity shocks of the global commodity market.

The current lag is critical: when the rupee devalues today, we feel the pinch in the retail fuel and logistics sector with a lead time of approximately one to two quarters. As one observer aptly noted on Reddit:

"A lot of people are treating the move in USD/INR like some sudden collapse event, but the pressure had been building for months in plain sight. Oil kept climbing, FIIs kept pulling money out, and geopolitical stress only made investors move harder toward safe assets."

— u/macro_analyst, r/indianeconomy

RBI Intervention vs. Market Reality

The Reserve Bank of India (RBI) has historically maintained a policy of 'managed volatility,' stepping in to prevent free-falls. However, there is a fundamental constraint to this approach. While forex reserves are substantial, they are not infinite. Defending the currency against a sustained, structural trend—rather than a temporary liquidity crunch—is akin to plugging a dam with one’s fingers.

Market participants are increasingly skeptical of whether intervention can offset the broader trade deficit. While industrial policy aims to boost the 'Make in India' initiative to increase exports, the import bill for essential goods—crude oil, refined electronics, and edible oils—continues to grow faster than our current export capacity. Unless India can aggressively de-link its energy consumption from fossil-fuel imports, the RBI’s battle remains defensive at best.

The Road Ahead: Is a Pivot Possible?

Stabilizing the rupee requires more than just currency management; it demands an aggressive structural pivot. If the current trajectory continues, India faces the risk of imported inflation becoming a permanent fixture of its economic landscape.

Policy experts argue that the roadmap to stability must prioritize three pillars:

1. Accelerated Decarbonization: Moving beyond rhetoric to force-multiply solar and hydrogen infrastructure to cut the oil bill.

2. Export Value-Addition: Shifting from a raw-material import/low-end assembly model to high-value manufacturing that can actually challenge the trade deficit.

3. Forex Diversification: Reducing the over-reliance on USD-denominated trade settlements.

The Bottom Line

The breach of the 96-mark is a wake-up call. The rupee’s weakness is a symptom of a larger, systemic vulnerability. While central bank intervention provides a temporary buffer, the only long-term hedge against a depreciating currency is an economy that imports less of what it consumes. Until then, the '100' threshold will continue to hang over the economy like a Damocles sword, testing the resolve of both policymakers and the public.