The Global Portfolio: Why Indian Gen-Z Is Looking Beyond Domestic Equities

Driven by skepticism toward the domestic economy, India's tech-savvy youth are increasingly diversifying into USD-denominated assets. We explore whether this move toward global exposure is a prudent hedge against currency depreciation or a reaction to market alarmism.

Photo by Ravi Roshan on Pexels

The Global Portfolio: Why Indian Gen-Z Is Looking Beyond Domestic Equities

For a generation of Indian investors who cut their teeth on the post-pandemic bull run, the 'India Growth Story' has been the gospel. Yet, beneath the veneer of record-breaking Nifty 50 highs, a subtle but tectonic shift is occurring. Driven by a cocktail of macroeconomic anxiety and the ease of digital-first finance, India’s tech-savvy youth are increasingly looking past the borders, pivoting their portfolios toward USD-denominated assets. This isn't just about chasing Apple or Nvidia; it’s a calculated, if sometimes alarmist, insurance policy against the long-term slide of the Indian Rupee.

The Rise of the Global Investor

Historically, Indian investors have suffered from a severe 'home bias.' The comfort of the familiar has long dictated capital allocation. However, Gen-Z and younger Millennials are increasingly treating geographical diversification as a mandatory risk-mitigation tool rather than an optional luxury. This transition is fueled by a pervasive skepticism toward domestic macroeconomic stability.

Social media platforms have become incubators for this sentiment, where 'doom-scrolling' often blends with legitimate economic analysis. Whether it is grounded in reality or fueled by digital echo chambers, the sentiment is clear: for many, the domestic market no longer feels like a safe harbor.

"INR is depreciating badly against the USD for decades now - USD touched 96 INR today! A dumb patriot like me kept investing in Indian stocks for the last 5 years... feels like I was dumb to not diversify my portfolio." — u/FinancialSeeker, r/IndianStreetBets

Currency Depreciation: Hedge or Hype?

At the heart of this exodus is the depreciating Rupee. Investors are asking whether global exposure is a formal hedge or merely a way to lock in USD-denominated growth. Economists often argue that since stocks are real assets, their nominal prices tend to adjust upward in local currency terms during periods of inflation or depreciation, providing a 'natural' buffer.

""The currency doesn't really matter. Since stocks are real assets, their prices automatically rise in nominal terms during a currency depreciation anyway." — Top Comment, r/SwissPersonalFinance

Despite this, the psychological weight of holding assets in a hard currency remains a massive draw. For the retail investor, the goal isn't just growth; it is the decoupling of their net worth from the volatility of a single emerging market economy.

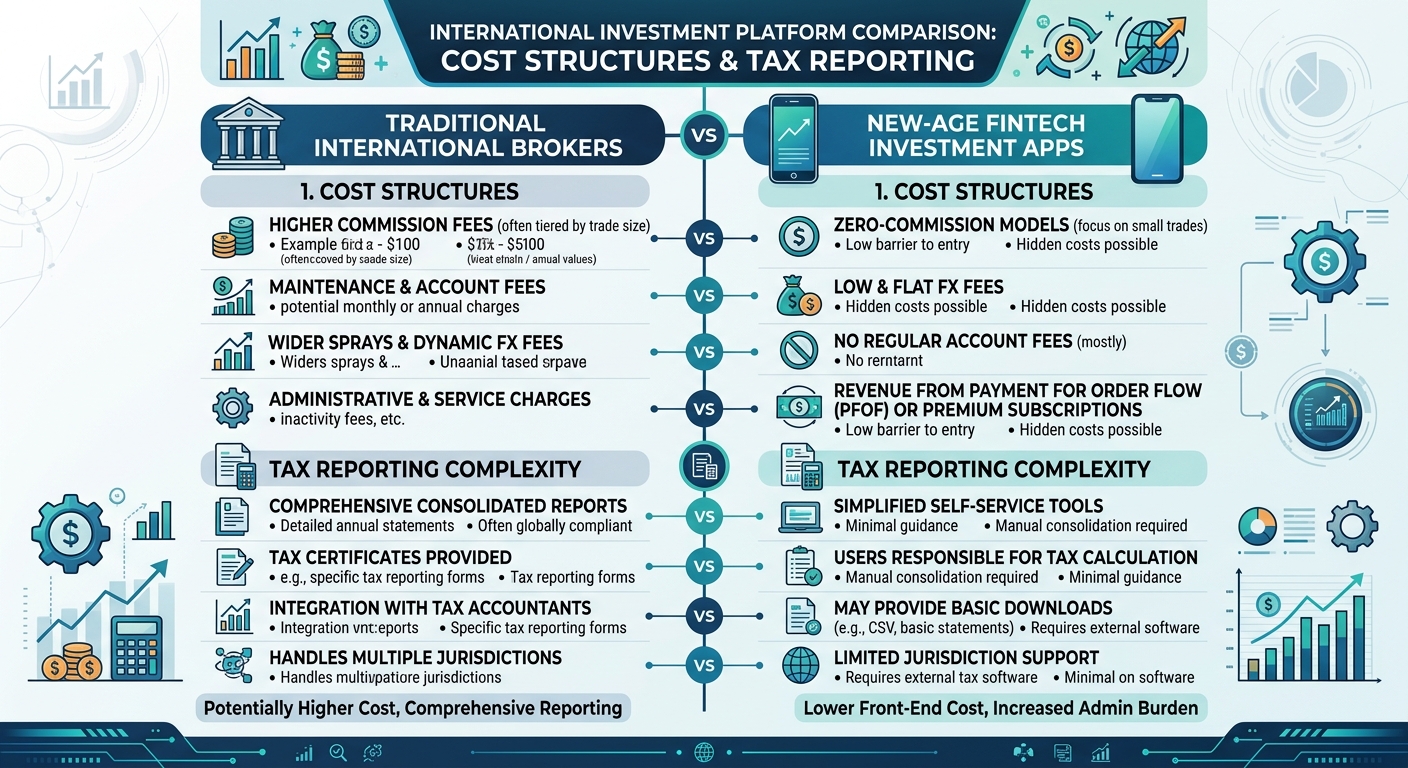

Navigating the Logistics: Brokers, Fees, and Taxes

Transitioning from local to global requires navigating the Reserve Bank of India’s Liberalised Remittance Scheme (LRS). Under LRS, individuals can remit up to $250,000 per financial year, but the compliance burden often feels daunting. Modern fintech platforms have made this journey seamless, though not necessarily cheap.

Investors often find themselves caught in a trade-off: use a low-cost, global-standard broker like Interactive Brokers, which requires more administrative heavy-lifting, or opt for domestic fintech apps that simplify the UI but levy hidden costs in currency conversion and maintenance fees.

When shifting brokers, the advice is clear: avoid liquidation if possible.

"Don't sell and withdraw unless you plan to exit your positions. Also, if you get it back to your Indian account, you'll pay forex charges, TWICE! Just transfer your brokerage." — u/InvestAbroad, r/IndianStreetBets

Furthermore, Indian tax residents must be cognizant of the Tax Collected at Source (TCS) under the LRS, which has been a major point of friction, alongside the long-term capital gains tax implications of holding international assets.

Strategic Allocation: The Path Forward

Building a balanced portfolio isn't about abandoning India; it is about acknowledging that the world is larger than any single index. A sensible approach for the modern investor is to allocate 10% to 20% of a portfolio toward global indices, such as the S&P 500 or Nasdaq-100, through low-cost ETFs.

This provides the necessary currency hedge without sacrificing the potential alpha of the domestic market. For beginners, the path forward is to focus on dollar-cost averaging into global ETFs, minimizing the impact of exchange rate volatility over the long term.

Bottom Line

The pivot toward global equities is a reflection of a maturing investor base. While the anxiety surrounding the Rupee is often amplified by social media, the underlying strategy of geographical diversification is sound financial practice. By treating the global market as a portfolio component rather than an exit strategy from the Indian economy, Gen-Z investors are building a more resilient financial future.