The 'Influencer vs. Reality' Trap: Is 1.5Cr the New Entry-Level for Indian Urban Homes?

Personal finance creators are preaching the 'rent-and-invest' gospel, but in India's metros, the ground reality of land-backed price floors tells a different story. We investigate why 1.5Cr no longer buys a premium lifestyle and whether the 'always-up' real estate narrative is finally breaking.

Photo by Rajkumarrr comics on Pexels

The 'Influencer vs. Reality' Trap: Is 1.5Cr the New Entry-Level for Indian Urban Homes?

In the polished, high-definition world of Indian personal finance creators, the gospel is clear: rent, invest the surplus in index funds, and avoid the "debt trap" of an Indian home at all costs. But walk into a sales gallery in Gurugram, Bengaluru, or Mumbai, and you are met with a jarringly different reality. Here, 1.5 crore is no longer the ticket to a luxury lifestyle; it is the entry-level baseline for a standardized 2BHK in a decent, connected neighborhood.

This disconnect between digital advice and market physics has created an 'affordability trap.' Mid-career professionals, buoyed by rising salaries, find themselves squeezing into massive 20-year EMI commitments, not necessarily because they want to build an asset, but because the alternative is being pushed further and further into the urban periphery.

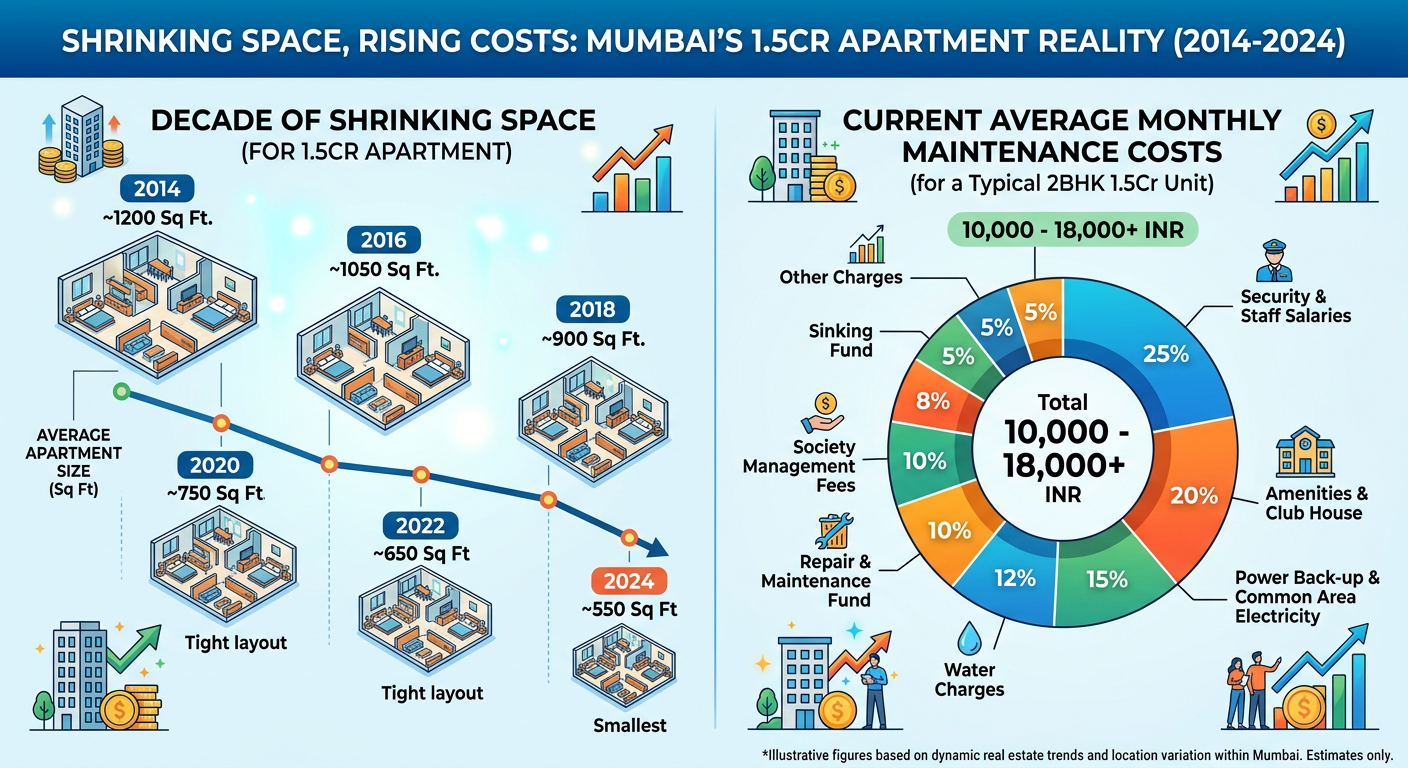

The 1.5 Crore Mirage: Redefining Premium

Not long ago, a 1.5 crore budget commanded a premium apartment with sprawling balconies and park views. Today, that same capital buys you a 'compact' unit in a high-density redevelopment project. Developers have pivoted their strategy entirely: by optimizing floor-space indices (FSI) and layering projects with "wellness" amenities—think smart-automation, yoga decks, and clubhouses—they have successfully rebranded smaller footprints as "micro-luxury."

This strategy is deliberate. By catering to high-income, stability-seeking professionals, builders have effectively abandoned the price-sensitive middle class. The result is a market where the entry-level price for "respectable" urban living has inflated by nearly 30-40% over the last four years.

Influencer Rhetoric vs. Market Mechanics

Personal finance influencers often advocate for the mathematical superiority of renting. They argue that the yield on residential property—often a paltry 2-3% annually—is a poor substitute for equity markets. Yet, they consistently overlook the "psychological security" factor embedded in the Indian cultural psyche.

"I keep reading threads about how renting is smarter, but my landlord just decided to sell the flat I've lived in for three years. That 'financial efficiency' doesn't help when you're moving your entire life every 24 months. The mental tax is real." — @UrbanRenterDelhi, X

While digital discourse suggests a bubble waiting to burst, developer balance sheets tell a different story. In India, real estate is rarely a truly open market; it is a liquidity-trapped ecosystem. Deep-pocketed developers and cash-rich investors ensure that price floors remain stubbornly high, preventing the "crash" that many online commentators perpetually predict.

The Hidden Cost of Legacy vs. The Convenience of Townships

For those choosing between old-world charm—like the legacy pockets of South Delhi or Bandra—and modern townships, the choice is increasingly financial rather than aesthetic. Retrofitting an aging property to modern safety and efficiency standards often costs 15-20% of the property value within the first five years.

Conversely, modern townships offer standardized maintenance, fire safety, and integrated infrastructure. While the "cost-to-space" ratio is better in satellite hubs, the commute time acts as a "hidden tax" on the professional’s time. The trade-off is increasingly binary: pay with your money for a smaller, modern unit in the center, or pay with your time for a larger space on the city's outskirts.

Does the Market Ever Actually Fall?

The dogma that "real estate never falls" is the most debated narrative in Indian finance. Whether it is an anomaly or simply an inflation-adjusted reality remains to be seen. In practice, Indian real estate rarely sees nominal price drops; it sees "time-corrections," where prices stagnate for half a decade while inflation and wage growth eventually catch up.

Because the market is driven by owners with low leverage compared to Western counterparts, there are few "distress sales" that would trigger a price collapse. For most Indians, buying a home is not just an asset allocation decision; it is a lifestyle hedge against the rising cost of urban living.

Bottom Line: The 'Use' vs. 'Investment' Divide

The fundamental error in the current debate is treating home-for-use as an investment product. If you buy a house to live in, you are purchasing a service (shelter) that comes with an option to own. When viewed through this lens, the 1.5 crore "entry-level" requirement is less about ROI and more about the price of admission to a specific standard of modern Indian urban life. The market is not broken; it is merely serving a new, more expensive definition of what it means to be "settled."