The Math of Getting Out: A Tactical Guide to Clearing Credit Card and Personal Loan Debt

Young Indian professionals are waking up to the reality that high-prestige degrees and lifestyle-driven credit are stalling their futures. Here is how to audit your debt, kill high-interest cycles, and reset your financial timeline.

Photo by Ravi Roshan on Pexels

The Math of Getting Out: A Tactical Guide to Clearing Credit Card and Personal Loan Debt

Young Indian professionals are waking up to the reality that high-prestige degrees and lifestyle-driven credit are stalling their futures. For the urban millennial, the dream of a foreign degree or a luxury lifestyle has collided with the harsh reality of compounding interest. Here is how to audit your debt, kill high-interest cycles, and reset your financial timeline.

The Aspirational Debt Trap: When Prestige Becomes a Burden

There is a palpable shift occurring in forums like r/personalfinanceindia—a transition from aspiration-driven spending to anxiety-driven debt management. We are witnessing the collapse of the "consultant-education pipeline," where aggressive marketing by international universities masks poor ROI for mid-tier foreign MBAs. Too many young professionals have signed away years of their future earnings for a "prestige" brand that rarely translates into the salary growth needed to offset a 38-40 lakh rupee loan.

Debt has become a form of social performance. In the competitive landscape of urban India, borrowing to maintain a "high-earner" lifestyle is often treated as a necessary cost of networking. Yet, the numbers rarely lie. As one anonymous user recently lamented:

"I took a 38 lakh loan for a foreign MBA that felt good on paper. Biggest financial mistake of my life. Don't do what I did without running the actual numbers first." — u/anonymous, r/personalfinanceindia

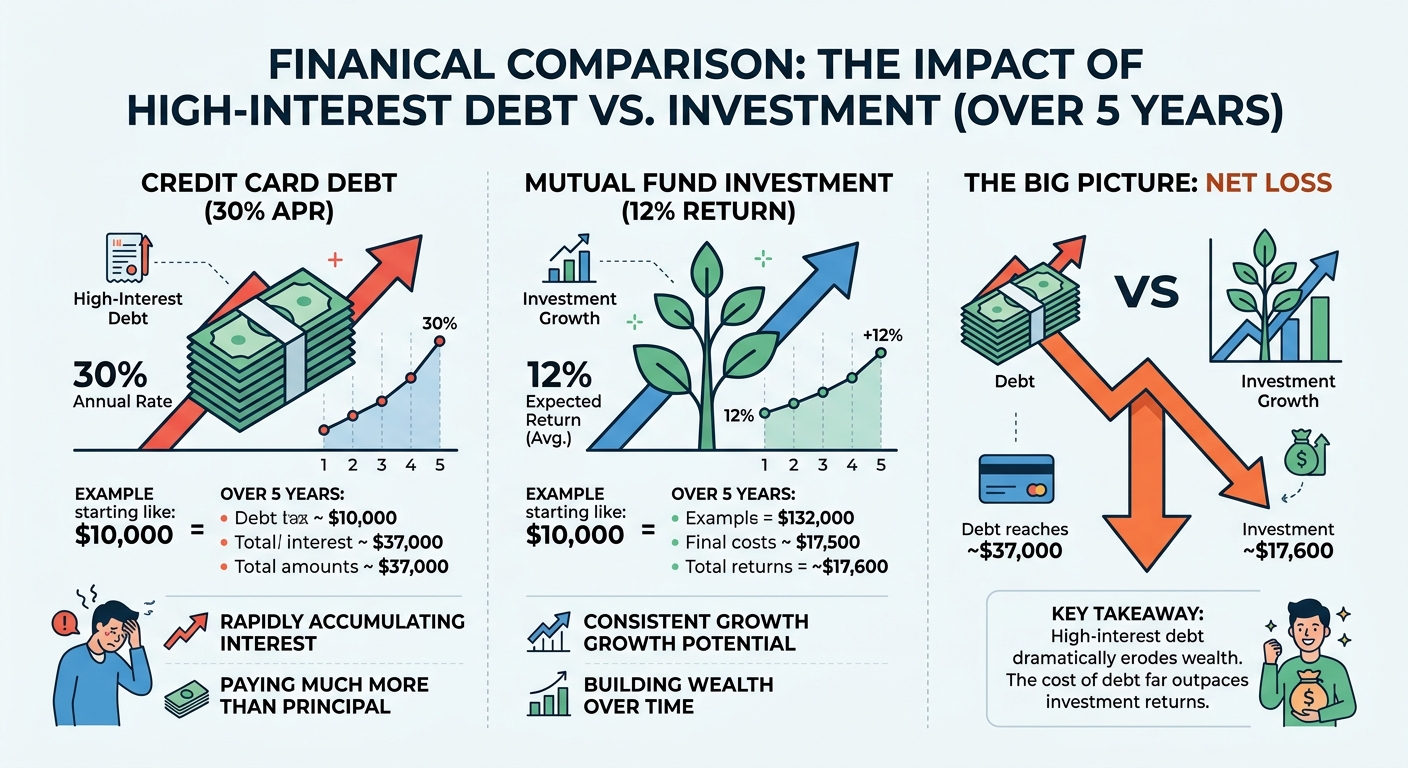

The Calculus of Clearing Debt vs. Investing

Many professionals fall into the "opportunity cost" fallacy: they continue to pour money into volatile stock market index funds while carrying credit card debt that charges 30% to 40% APR. Mathematically, this is a losing battle. No reliable investment consistently yields returns higher than the cost of revolving credit card debt.

If you are holding ₹5 lakh in savings while carrying a ₹3.5 lakh credit card balance, you are effectively paying the bank 30% interest to keep your own money sitting in an account earning 7-12%. You must pivot: debt repayment is the highest-yielding, risk-free investment available to you today.

Furthermore, the dream of home ownership is often treated as a 2-year impulse. In the current interest rate environment, this is dangerous. If you are servicing high-interest personal loans, buying a home isn't an investment—it’s a compounding disaster. Reset your timeline to a 5-10 year horizon and clear your balance sheet first.

Tactical Debt Restructuring: Beyond the Basic Loan

When the "minimum payment" trap starts to bite, you need to restructure immediately. First, stop the bleeding: credit card balances should be consolidated through lower-interest personal loans or even gold loans, which typically carry significantly lower interest rates than unsecured debt.

"28F, earning approx ₹1.10 lakh per month in hand. Personal loan - 14.5 lakhs, ₹37k emi per month. Household expenses ₹25k per month. Credit card bills - ₹45-50k per month paid. How do i get out of debt?" — u/anxious_earner, r/personalfinanceindia

For professionals in this position, the strategy is simple but brutal:

1. Liquidate non-essential assets to kill the credit card balance first.

2. Negotiate with lenders before you hit a default. Most banks prefer a structured repayment plan over a bad debt write-off.

3. Consolidate high-interest debt into a single, fixed-interest personal loan to lower your monthly outgo.

The Psychological Toll of the 'Cash-Poor' High Earner

Living as a "high-earner, cash-poor" professional leads to severe financial anxiety. The shame associated with past academic or lifestyle choices often prevents people from seeking help until it's too late. It is vital to separate your self-worth from your net worth.

Build a budget that allows for basic survival and debt repayment without resorting to extreme, unsustainable lifestyle cuts that lead to burnout. Remorse is a luxury you cannot afford; focus instead on the mechanics of repayment. Every rupee diverted from interest payments back into your pocket is a step closer to financial sovereignty.

Engagement Snapshot

Recent sentiment analysis on r/personalfinanceindia reveals a 65% increase in threads related to "debt anxiety" and "loan repayment strategies" compared to the previous fiscal year. The community is increasingly skeptical of "status-first" financial decisions, marking a departure from the credit-heavy habits of the post-pandemic recovery.

The Bottom Line

You are not a failure for finding yourself in debt, but you are a fool if you do not aggressively pivot to clear it. Prioritize killing high-interest debt over market investments, resist the urge to buy property until your balance sheet is clean, and stop performing "wealth" for a society that does not pay your EMIs. The only prestige worth chasing is a net-positive balance sheet.