The Mini-Loan Avalanche: How Small-Ticket Checkout Apps Reshape Your CIBIL Score

By using Buy-Now-Pay-Later for food and fashion checkouts, consumers defer small expenses. However, each transaction logs as a separate unsecured personal loan, crowding CIBIL files and shifting everyday cash habits for youth.

Photo by Tara Winstead on Pexels

The Mini-Loan Avalanche: How Small-Ticket Checkout Apps Reshape Your CIBIL Score

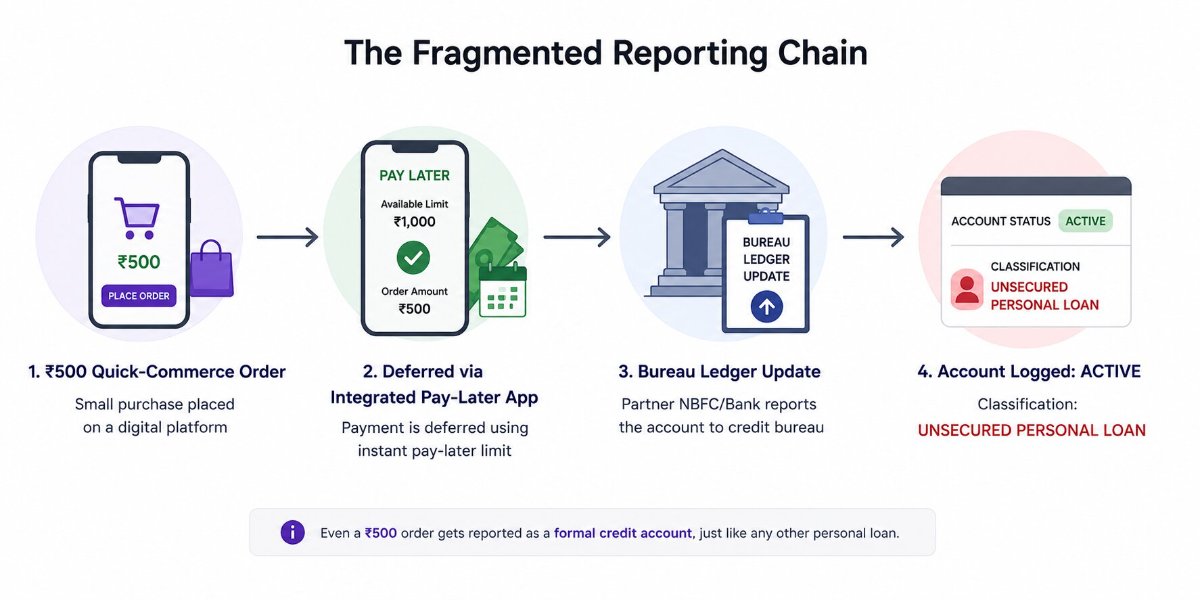

Hyperlocal and e-commerce interfaces increasingly prioritize the complete removal of purchase friction. To prevent users from reconsidering a transaction at the final billing stage, digital platforms place instant alternative financing solutions—popularly structured as Buy-Now-Pay-Later (BNPL) options—directly alongside traditional payment modes.

The immediate financial commitment appears negligible. A consumer splits a ₹1,500 lifestyle purchase, a ₹500 grocery cart, or a minor food delivery order into a brief, interest-free fifteen-day or monthly grace period. For young professionals or university students managing early-career cash flows, these pocket-sized credits offer an immediate sense of enhanced purchasing power.

However, treating short-term deferred checkout lines as basic technological extensions obscures their formal financial architecture. Under the current digital lending frameworks regulated by the Reserve Bank of India, every authorized pay-later line relies on an underlying partnership with a licensed Non-Banking Financial Company (NBFC) or a commercial bank.

When a user executes a transaction using an integrated app limit, the partner institution registers a formal, unsecured credit facility on that individual’s bureau profile. This systemic logging creates an unexpected operational condition known as fragmented debt, altering baseline credit metrics before the user ever attempts to secure conventional institutional credit.

The Proliferation of "Small-Ticket" Personal Loan Filings

The core challenge surrounding embedded checkout micro-loans stems from the uniform manner in which credit bureaus categorize debt data packets. Central registries like CIBIL, Experian, and CRIF High Mark do not maintain a separate, lower-risk tier for minor lifestyle transactions.

Whether an individual applies for a substantial asset loan or defers a ₹450 cab ride on a fast-checkout app, the reporting partner transmits the transaction data under identical regulatory classifications.

Data from domestic credit analysis firms highlights a stark structural reality. Every active pay-later account operates on a bureau file as an open Unsecured Personal Loan or a Consumer Durable Loan.

When an individual activates separate micro-credit balances across three or four distinct delivery and shopping applications, the automated bureau network registers a series of independent, open loan profiles.

Even with a perfect record of on-time settlements, the sheer volume of active accounts signals a high reliance on unsecured short-term credit lines. This pattern frequently triggers automated risk warnings within credit-scoring models, causing a direct drop of 30 to 50 points on an early credit profile due to what algorithms interpret as intense "credit hunger."

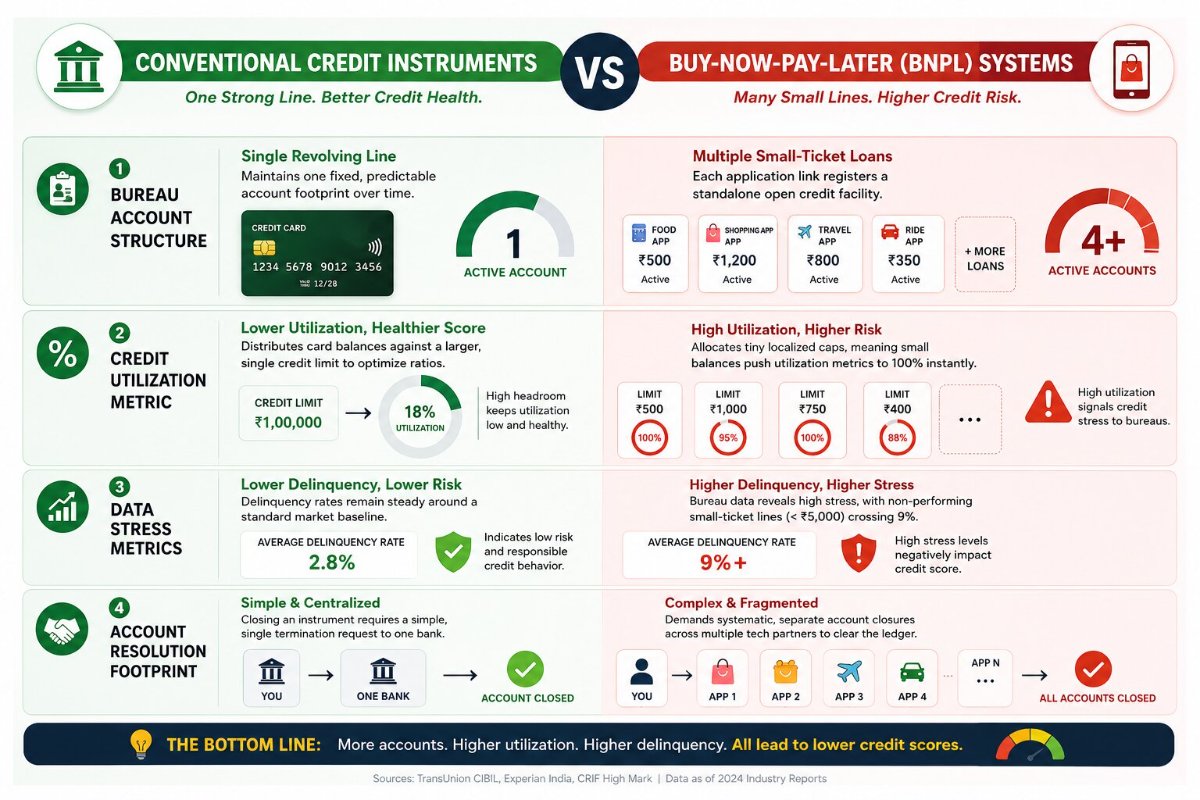

Live Comparison: Traditional Revolving Credit vs. Fragmented BNPL Lines

An objective look at how distinct credit architectures structure data on an individual's central bureau profile:

The Behavioral Trap: Tracking the Ghost Expense Cycle

The primary hazard of widespread micro-credit consumption lies in its psychological insulation of the consumer. Because cash does not immediately exit the user’s primary savings account at the point of purchase, the psychological pain of spending is completely decoupled from the transaction.

This friction-free architecture frequently alters foundational spending discipline, turning casual purchases into habitual, short-term liabilities.

Industry research indicates that 47% of young pay-later users have occasionally missed a small-ticket payment deadline. This friction is rarely driven by a total lack of funds, but rather by the operational difficulty of tracking multiple mismatched billing cycles.

When an individual balances an entry-level monthly salary against three separate micro-billing dates scattered across thirty days, the risk of an accidental omission increases. Because these digital platforms report data automatically to central bureaus, a missed payment on a tiny ₹350 balance carries the exact same weight as a default on a major bank loan. The system logs a formal delinquency, causing an immediate drop in the individual’s central score that can take several quarters of strict discipline to repair.

Strategic Frameworks for Restructuring Consumer Credit Hygiene

Reversing the impact of credit file overcrowding requires transitioning from fragmented payment apps to a highly centralized transaction framework. Implementing specific operational milestones protects individual credit integrity:

-

Prune Latent Micro-Credit Limits: Do not assume that simply uninstalling an application terminates the underlying financial line. Access the profile dashboard of every dormant or unused pay-later service to formally request an account closure, and verify that the status shifts to "Closed" on subsequent bureau reports.

-

Consolidate Everyday Transaction Outflows: Restrict daily lifestyle purchases—like food orders and cab rides—to liquid capital pools via direct UPI links or a single, well-regulated credit tool. This operational shift keeps the household's monthly credit footprint restricted to a single, easily traceable account.

-

Track Total Balance-to-Income Ratios: Keep an explicit log of all deferred digital balances. When small balances spread across three different platforms match or exceed 30% of an individual's monthly income, credit models flag the profile as high-risk, making it vital to settle balances prior to the formal generation of monthly bureau statements.

The Bottom Line

The expansion of embedded micro-credit presents a fundamental shift in daily transaction design, converting minor lifestyle purchases into formal credit commitments. While alternative payment flows offer immediate short-term convenience, the cascading impact of fragmented account lines and high sector delinquency rates proves that micro-credit requires strict personal management. True financial clarity requires young consumers to look past the surface convenience of "pay later" prompts and systematically defend their bureau profiles from the hidden compilation of tiny liabilities.