The 'Perfect SIP Date' is a Myth: Why Your Calendar Isn't Your Portfolio Manager

Retail investors often obsess over choosing the 'best' date to execute a Systematic Investment Plan, hoping to gain a slight edge. Data reveals this pursuit is a fallacy, highlighting that behavioral consistency matters far more than predictive precision.

The 'Perfect SIP Date' is a Myth: Why Your Calendar Isn't Your Portfolio Manager

Retail investors often find themselves paralyzed by a peculiar form of financial perfectionism: the obsession with choosing the 'best' date to execute a Systematic Investment Plan (SIP). Whether it’s aiming for the 5th of the month to catch a salary-day dip or the 15th to capitalize on mid-month volatility, the hope is that a minor tactical advantage will compound into a massive portfolio lead. Data reveals this pursuit is a fallacy, highlighting that behavioral consistency matters far more than predictive precision.

The Core Blueprint: A Lesson in Radical Pragmatism

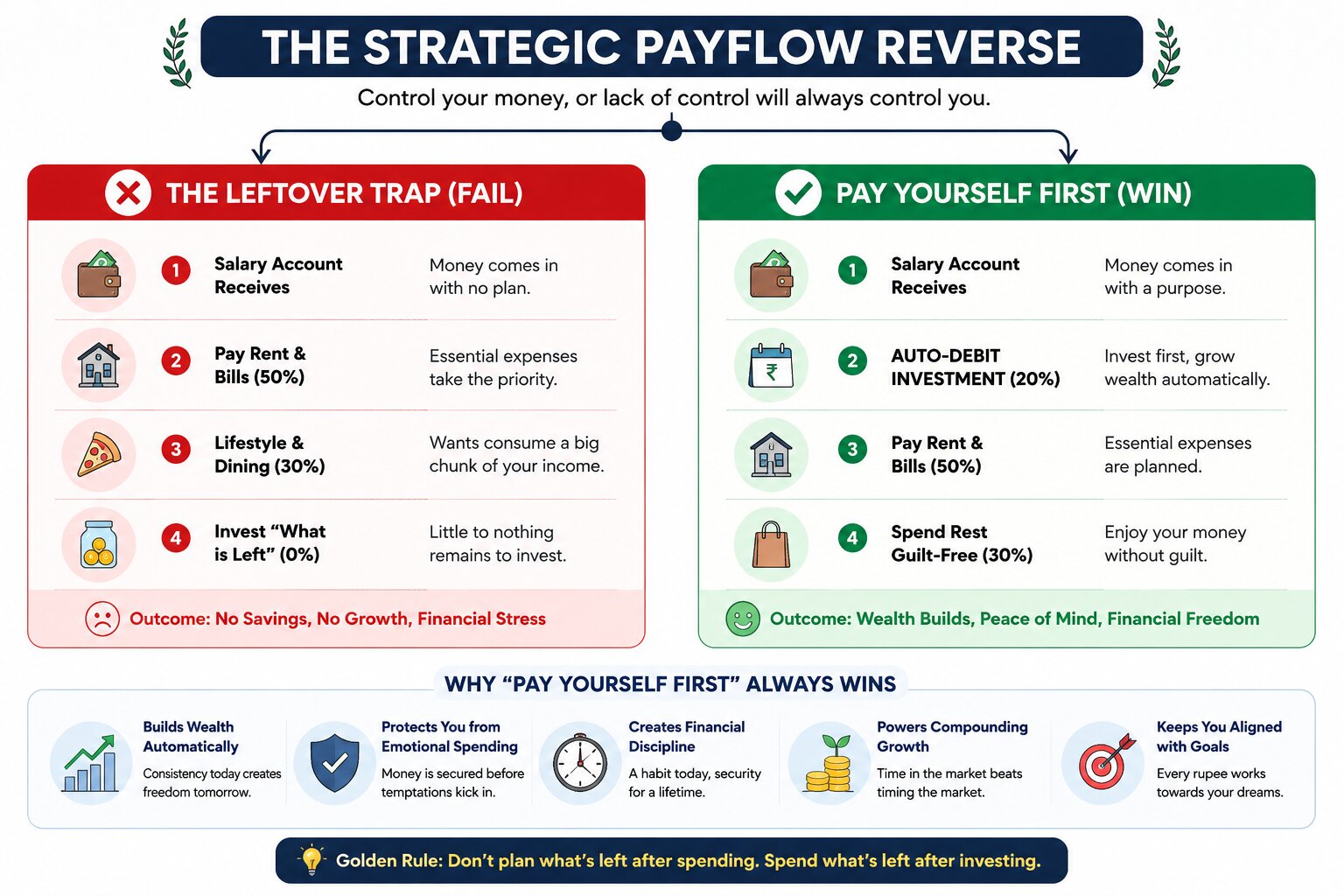

To understand why searching for a "perfect date" is an operational bottleneck, we have to look at baseline personal finance architecture. A cornerstone rule of thumb used by wealth planners worldwide is the 50-30-20 rule: allocating 50% of your take-home pay to essential needs, 30% to discretionary lifestyle wants, and a non-negotiable 20% toward long-term savings and investments.

The fatal mistake most young professionals make is treating that 20% allocation as an afterthought—investing whatever happens to be left over at the end of the month. True financial discipline flips this sequence entirely through a principle known as "Paying Yourself First."

The moment your income hits your account, your 20% investment slice should be mechanically moved out via automation before you have a chance to touch it. This simple protocol protects your capital from emotional spending biases. Yet, it is precisely at this automation step where investors fall into the trap of calendar optimization—wasting valuable time trying to pick the perfect date for the debit to trigger.

The Illusion of Optimization

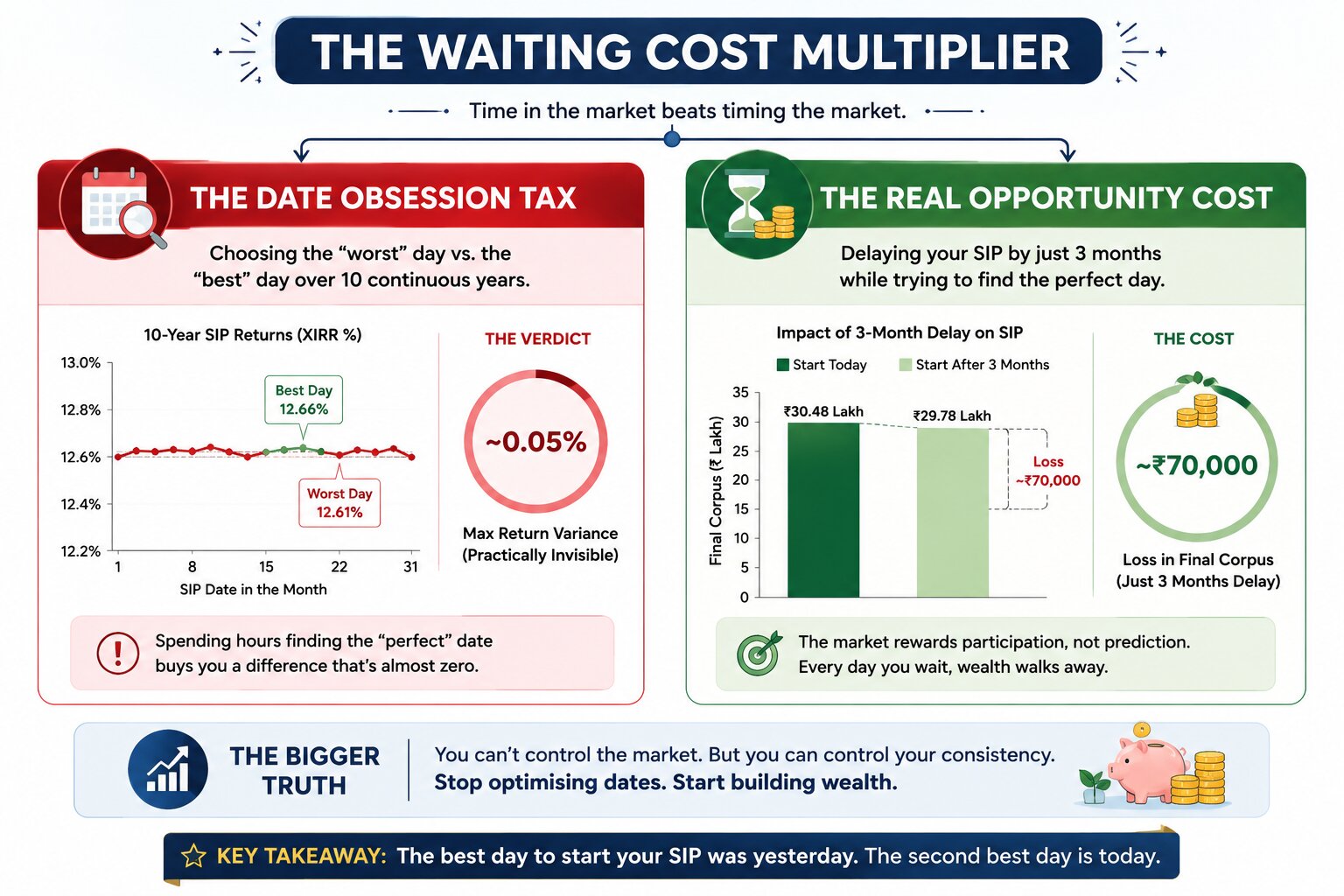

The digital age has armed the average retail investor with sophisticated charting tools and backtesting data. However, this has birthed a new problem: analysis paralysis. Investors spend hours debating the optimal entry date, unaware that the empirical difference is statistically trivial.

Institutional research consistently demonstrates that the difference in Extended Internal Rate of Return (XIRR) between various SIP start dates is practically invisible over a long-term horizon. By obsessing over the calendar, investors are effectively trading their time for a gain that wouldn't cover a modest brokerage fee.

The Hard Numbers: 10-Year Rolling Returns Matrix

To systematically debunk the "perfect date" fallacy, let's look at the comprehensive, long-term rolling data updated through 2026. The table below maps the 10-Year Average SIP Rolling Returns (% XIRR) across every single calendar day for the S&P BSE Sensex TRI from September 1996 to the present day.

10-Year Average SIP Rolling Returns Matrix (Updated 2026)

| Monthly SIP Date | 1 | 2 | 3 | 4 | 5 | 6 | 7 |

|---|---|---|---|---|---|---|---|

| SIP Return (% XIRR) | 12.64% | 12.63% | 12.63% | 12.61% | 12.61% | 12.60% | 12.60% |

| Monthly SIP Date | 8 | 9 | 10 | 11 | 12 | 13 | 14 |

| SIP Return (% XIRR) | 12.60% | 12.59% | 12.59% | 12.60% | 12.61% | 12.62% | 12.62% |

| Monthly SIP Date | 15 | 16 | 17 | 18 | 19 | 20 | 21 |

| SIP Return (% XIRR) | 12.63% | 12.62% | 12.64% | 12.63% | 12.63% | 12.63% | 12.63% |

| Monthly SIP Date | 22 | 23 | 24 | 25 | 26 | 27 | 28 |

| SIP Return (% XIRR) | 12.64% | 12.64% | 12.63% | 12.63% | 12.63% | 12.62% | 12.62% |

Source Baseline: WhiteOak Capital Mutual Fund Internal Research. 10 Years Average SIP Return (% XIRR) on a daily rolling basis for individual calendar dates for S&P BSE Sensex TRI (September 1996 to 2026). Past performance is not a guarantee of future returns.

The data reveals that the numbers across all 28 days move virtually in lockstep. The maximum spread between the absolute peak day (the 1st, 17th, 22nd, or 23rd at 12.64%) and the absolute lowest day (the 9th or 10th at 12.59%) is a mere 0.05%.

For an investment profile, that minor fraction translates to a trivial difference over a decade. Meanwhile, holding back your cash for just a few months to wait for a "market dip" or a perfect entry point can slash your final corpus significantly due to missed compounding. The cost of delaying your entry is drastically more expensive than the choice of the calendar date itself.

Psychology Over Strategy: The 2026 Reality Check

If the math is so clear, why do so many retail investors abandon their SIPs during sideways patches? The answer lies in the psychological shift when consecutive years of spectacular bull runs suddenly give way to extended range-bound volatility, as seen throughout the consolidation phases of 2026.

Many investors who entered during the atypical pandemic bull run became conditioned to expect immediate double-digit validation. When the market moves sideways or experiences localized corrections, the emotional urge to pause the SIP "until things clear up" spikes.

This is where true discipline proves its value. When the market cools or drops, a fixed monthly SIP auto-debit quietly buys more mutual fund units at lower values. Pausing or trying to manually time these phases breaks the rupee-cost averaging loop, meaning you completely miss out on cheap accumulation windows that fuel the next major macro leg upward.

Radical Pragmatism: A New Framework

Traditional sector rotation and complex market timing models are showing declining utility for retail participants navigating high-frequency, algorithm-driven markets. The solution is absolute operational automation.

Automation acts as the ultimate hedge against human cognitive bias. By removing the need for daily, weekly, or even monthly decision-making, you insulate your capital from your own emotional impulses.

The Bottom Line

The myth of the 'perfect SIP date' survives because it promises control in a market environment that offers none. True wealth creation isn't found in a spreadsheet row comparing the 5th vs. the 25th; it is found in the quiet, mechanical act of showing up regardless of what the charts say.

The single best date for your SIP is a functional choice, not a strategic one: schedule it 2 to 3 days after your monthly income hits your account. Ensure the capital is safely deployed before discretionary spending takes over, let the automation run in the background, and let time handle the rest. Your calendar is for meetings; your SIP is for time in the market. Keep them separate.