The Postpaid Car: Inside the Pay-Per-Kilometer Battery Scheme Disrupting Indian EVs

A significant change is rolling out across Indian dealership floors. With top manufacturers adopting the Battery-as-a-Service (BaaS) ownership model, the entry price for popular electric vehicles has suddenly dropped by lakhs. But removing the battery from the sticker price transforms your vehicle layout into an ongoing monthly postpaid bill. We break down the real-world unit economics of car rentals, the usage math, and whether this new model truly saves your household budget.

Photo by Giant Asparagus on Pexels

The Postpaid Car: Inside the Pay-Per-Kilometer Battery Scheme Disrupting Indian EVs

A massive restructuring is quietly sweeping across showroom floors, upending how consumers purchase transport assets. For years, the high upfront acquisition premium of high-voltage lithium-ion packs choked mass market adoption. Buyers paid a heavy entry tax on Day 1 just to access the promise of low running costs.

Now, automakers are deploying a different playbook. Heavyweights like JSW-MG, Tata, Maruti Suzuki, and Kia are aggressively rolling out Battery-as-a-Service (BaaS) platforms. This structural shift decouples the battery from the vehicle shell, transforming a heavy upfront asset purchase into an ongoing, postpaid utility commitment.

Consider the reality facing an urban buyer looking at a mid-size vehicle. Under standard pricing frameworks, a modern electric crossover commands an all-in ex-showroom sticker price near ₹14.10 Lakh. Step into a modern dealership utilizing the BaaS framework, and that same vehicle rolls off the lot for an upfront capital outlay of just ₹9.99 Lakh.

The financier assumes ownership of the internal 38 kWh battery pack. In turn, the buyer signs a contract committing to a running fee—typically ₹3.50 to ₹4.50 for every single kilometer recorded on the odometer. It instantly targets the psychological friction of high vehicle down payments, matching electric vehicle entry points directly with legacy petrol hatchbacks.

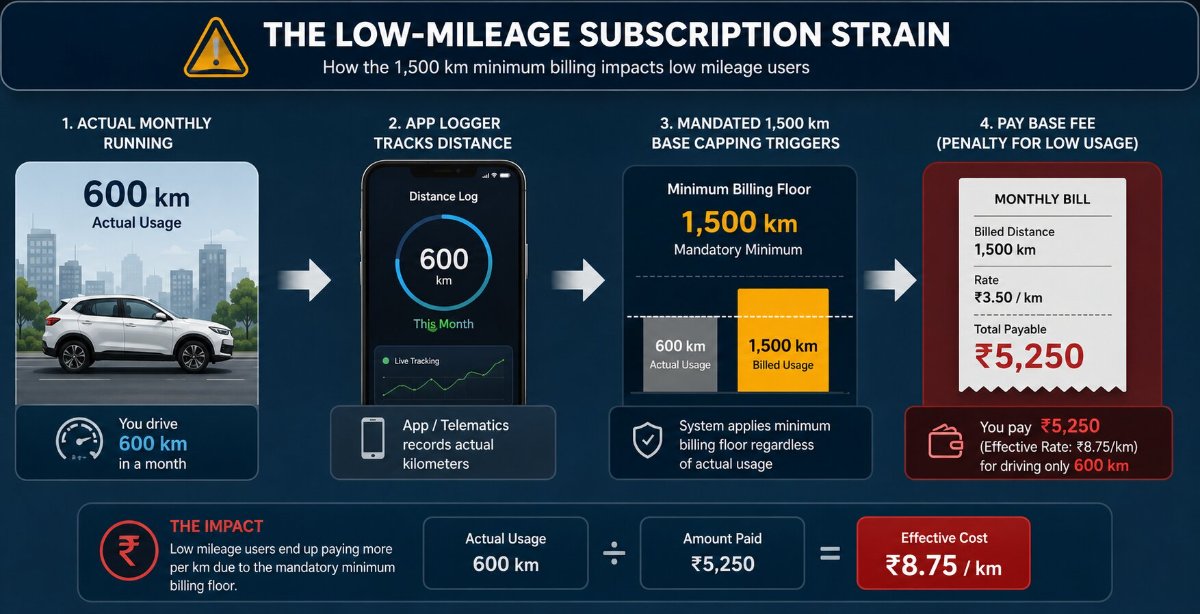

The 1,500-Kilometer Floor: When Low Mileage Becomes a Financial Penalty

The financial trap doors of this model emerge only when you audit the fine print governing these structured legacy agreements. Most consumers view "pay-as-you-go" frameworks as entirely flexible structures where zero driving equals zero billing.

The practical reality on the ground operates under a completely different logic. Major institutional financing lines—including Bajaj Finance and Hero Fincorp—protect their asset yields by embedding mandatory minimum distance floors directly into the lease paperwork.

If an urban professional utilizes a BaaS-backed vehicle strictly for short, local city commutes—clocking a mere 600 kilometers over thirty days—the billing portal ignores the lower distance. The automated system defaults straight to the mandated 1,500-kilometer base floor. At a baseline rate of ₹3.50 per kilometer, the owner faces a mandatory fixed outflow of ₹5,250. This artificial calculation instantly drives the real-world operational cost up to a steep ₹8.75 per kilometer before factoring in the actual electricity units consumed at the home wall box.

Live Comparison: The Active 2026 BaaS Playing Field

The structural options available to Indian car buyers have diversified significantly, with uniform usage rates scaling cleanly alongside the size of the vehicle segment:

Secondary Volatility: The Resale and Repossession Frameworks

Shifting a vehicle’s core component into a recurring rental structure introduces complex challenges for long-term asset management. Because the battery contract binds the consumer to an external financial entity, missing recurring monthly usage payments triggers aggressive compliance loops. If a buyer defaults on their battery ledger, repossession clauses grant the financing partner the legal authority to seize the entire physical vehicle to safeguard their high-voltage component.

Furthermore, the pre-owned car market faces an infrastructure bottleneck when handling these hybrid ownership lines. When a first-owner attempts to sell a BaaS vehicle, the incoming buyer does not simply purchase a clean, unencumbered asset. The new owner must clear the financier's formal credit onboarding checks to legally assume the ongoing pay-per-kilometer contract.

Alternatively, the seller must execute a complete battery buyout clause—paying off the remaining depreciated value of the cell block to convert the vehicle back into a traditional, all-inclusive asset before clearing the registration transfer.

Strategy Metrics for Tracking Long-Term Running Outflows

Navigating a postpaid transport framework requires moving away from casual consumer habits. Executing a highly systematic distance evaluation balances monthly cash flows effectively:

-

Verify Vendor-Specific Floor Exemption: Before signing a standardized delivery contract, review alternative financier options. Specialized EV-lending platforms frequently eliminate the 1,500-kilometer mandatory baseline requirement, allowing low-mileage city drivers to settle accounts based strictly on actual odometer data.

-

Calculate Your True Odometer Break-Even: If your regular household usage naturally tracks above 1,800 kilometers a month, step away from the subscription model entirely. High-mileage drivers optimize their returns far faster by paying the full battery premium upfront, freeing their long-distance runs from a perpetual per-kilometer operation tax.

-

Isolate Your Aggregate Charging Costs: Do not conflate your monthly battery lease payment with your actual fuel bill. You must still overlay your domestic electricity tariff units or public commercial DC fast-charging plaza transactions onto your monthly budget to track the true running expenditure of the vehicle.

The Bottom Line

The implementation of Battery-as-a-Service architecture reshapes the financial engineering of personal transport, successfully converting a heavy upfront capital asset into an ongoing operational utility line. For the casual city commuter seeking to bypass the high entrance premium of electric drivetrains, it provides an immediate, cash-flow-friendly gateway to modern technology. But before you lock in a subscription contract, pull out a calculator and map your true odometer realities - ensuring that trading upfront cash for a permanent postpaid monthly usage cycle actively protects your long-term wealth.