The SpaceX IPO Evolution: From Aerospace Pioneer to a $1.75 Trillion AI Infrastructure Play

SpaceX's long-awaited S-1 filing reveals a staggering $4.94 billion loss, obscured by the integration of xAI infrastructure. As the company preps for its $1.75 trillion IPO, investors are left questioning if this is a revolutionary aerospace pioneer or a over-leveraged, vibe-based bubble.

Photo by RDNE Stock project on Pexels

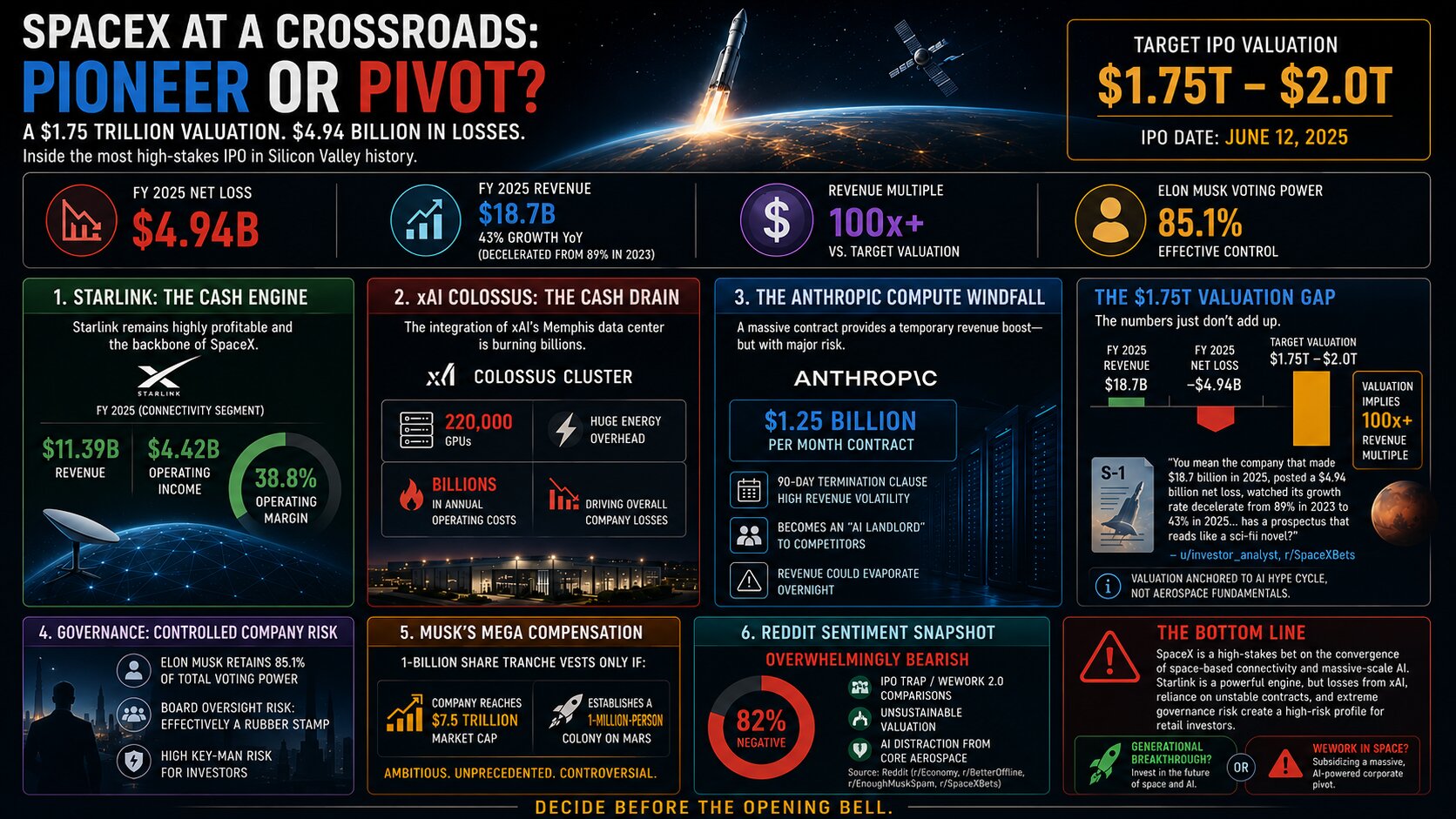

SpaceX’s long-awaited S-1 filing has finally hit the SEC portal, revealing a staggering $4.94 billion loss for the 2025 fiscal year. Masked by the aggressive integration of its xAI infrastructure and a massive, last-minute AI compute contract, the financials paint a picture of a company trapped between its identity as a legendary aerospace pioneer and its pivot into an over-leveraged, AI-centric valuation bubble. As the firm prepares for a historic $1.75 trillion IPO, investors are left questioning: is this a generational technological breakthrough, or the most high-stakes corporate pivot in Silicon Valley history?

The $1.75 Trillion Valuation Gap

SpaceX is targeting an eye-watering $1.75 trillion to $2 trillion valuation for its market debut. To justify this, the company points to its total addressable market in space, but the math tells a different story. With a $4.94 billion annual loss and decelerating growth, the valuation suggests an exorbitant 100x+ revenue multiple.

Critics argue that the valuation is largely a construct of the recent all-stock xAI merger, which artificially inflated the balance sheet to facilitate a massive public exit for early-stage investors. By folding the xAI “Colossus” data center operations into the SpaceX corporate umbrella, Musk has effectively anchored the company’s valuation to the current AI hype cycle rather than aerospace fundamentals.

"You mean the company that made $18.7 billion in 2025, posted a $4.94 billion net loss, watched its growth rate decelerate from 89% in 2023 to 43% in 2025... has a prospectus that reads like a sci-fi novel?" — u/investor_analyst, r/SpaceXBets

Starlink's Profitability vs. AI Infrastructure Burn

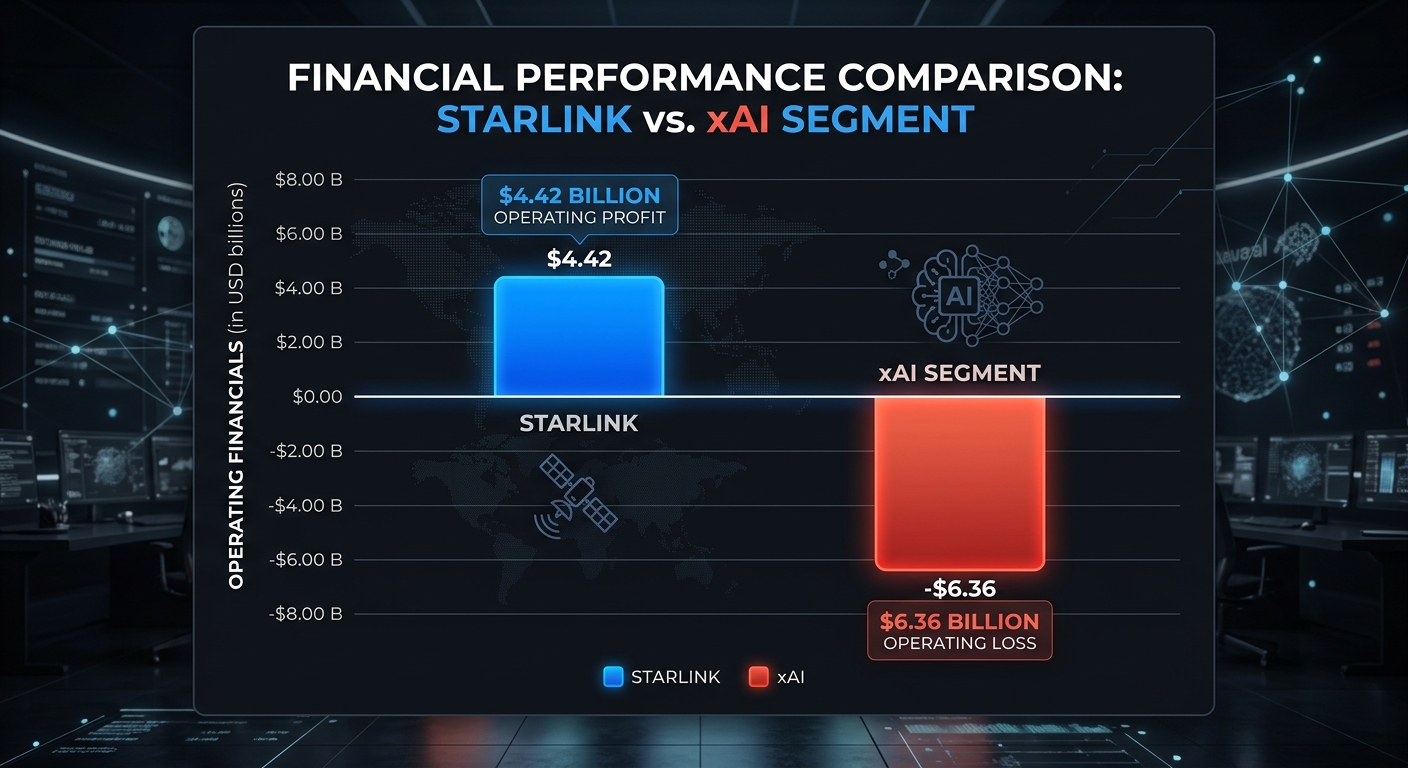

While SpaceX remains the undisputed king of orbit, its financial health is bifurcated. The Connectivity segment—Starlink—is a legitimate cash cow, generating $11.39 billion in revenue and $4.42 billion in operating income. However, this success is being systematically drained by the integration of the xAI “Colossus” cluster.

Operating the 220,000-GPU data center in Memphis is costing the company billions in operational expenses and energy overhead. For many, this is a strategic distraction. While Musk views AI compute as the logical next step for space-based infrastructure, shareholders are seeing a profitable aerospace company become a capital-intensive data center landlord overnight.

The Anthropic Compute Windfall

To bridge the cash flow gap, SpaceX has inked a massive $1.25 billion monthly contract with AI labs giant Anthropic. This deal positions SpaceX as a critical infrastructure supplier, essentially leasing its custom-built compute capacity to the very competitors that its sister company, xAI, is trying to defeat.

However, the stability of this revenue is precarious. The contract includes a 90-day termination clause, meaning the massive revenue windfall could evaporate if Anthropic shifts its infrastructure strategy or if market conditions for compute power sour. This turns SpaceX into a volatile "AI landlord" rather than a stable infrastructure utility.

Governance and the 'Controlled Company' Risk

Governance concerns are center stage in this prospectus. Elon Musk retains 85.1% of the total voting power, effectively rendering the board of directors a rubber stamp. The most controversial aspect is his compensation package: a 1-billion share tranche that only vests if the company hits a $7.5 trillion market cap and establishes a one-million-person colony on Mars.

"I hope no one buys stock. Please let people understand he's trying to unload this garbage pile onto the public so he doesn't have to admit he fucked the whole thing up." — u/tech_skeptic, r/EnoughMuskSpam

This structure mirrors the "key-man risk" that plagued WeWork, where personal ambition and corporate reality were tethered to unsustainable promises. For Indian institutional investors, who have recently shown interest in global space-tech, this level of concentration risk is a significant red flag that goes far beyond traditional market volatility.

Final Take: The Future of SpaceX May Depend on More Than Rockets

SpaceX is no longer being valued as a rocket company alone. It now represents a massive wager on the fusion of satellite connectivity, artificial intelligence, and hyperscale computing infrastructure. Starlink continues to prove that SpaceX can build highly profitable global platforms, but those gains are increasingly overshadowed by the enormous capital demands of xAI, volatile compute-leasing agreements, and a governance structure heavily concentrated around Elon Musk.

For investors, the June 12 IPO is more than a bet on space exploration — it is a referendum on whether SpaceX can successfully transform itself into the backbone of the AI economy without collapsing under the weight of its own ambition. The opportunity may be historic, but so is the risk.