The 'Zero-Tax' Pivot: Decoding India's Strategic Shift to Capture Long-Term Institutional Bond Flows

India has enacted the Income-tax (Amendment) Ordinance, 2026, effectively scrapping withholding taxes for foreign portfolio investors on government securities. This pivot marks a calculated maneuver to stabilize the rupee, deepen the domestic debt market, and decouple from volatile equity-driven capital flows.

The 'Zero-Tax' Pivot: Decoding India's Coordinated Framework to Anchor Global Capital

In a synchronized policy approach to manage capital flows, the Ministry of Finance and the Reserve Bank of India (RBI) have introduced a series of tax and regulatory updates. By coupling the newly issued Income-tax (Amendment) Ordinance, 2026, with comprehensive operational updates announced by RBI Governor Sanjay Malhotra during the June 5 monetary policy review, India has significantly restructured its framework for global debt investments.

This coordinated policy framework represents a strategic structural adjustment. Faced with shifting global allocation trends and notable outflows from emerging market equities, the financial leadership is optimizing its focus—rebalancing the nation's capital accounts by enhancing incentives for stable, long-term global bond investments.

Factors Driving the Global Equity Realignment

International institutional capital constantly adjusts its geographic footprint based on relative valuations and macroeconomic cycles. The current reduction in Indian equity holdings by global funds is primarily driven by three external factors:

- Reallocation to Specialized Tech Hubs: The global investment cycle is heavily weighted toward hardware artificial intelligence and advanced semiconductor manufacturing. Consequently, global managers are reallocating portions of their capital from broader emerging markets to manufacturing-heavy indices in East Asia.

- Normalized Valuations: Prior to the recent market corrections, domestic price-to-earnings multiples had risen significantly above historical averages, prompting standard profit-booking and portfolio adjustments by international asset managers.

- Competitive International Yields: Rising interest rates in western economies have driven risk-free yields on major global currencies above 4.3%. For conservative global pension and sovereign funds, these guaranteed international returns present a compelling alternative to emerging-market equities during periods of global uncertainty.

Macroeconomic Vulnerabilities of Variable Inflows

When international portfolios liquidate public equities at a rapid pace, the conversion of local currency into foreign currency for repatriation can create distinct pressures across the broader macroeconomic spectrum:

- Currency Adjustments: Heavy, localized demand for foreign currency can cause the exchange rate to adjust downward, with the Indian Rupee reaching a low of 96.96 per USD before stabilizing under active central bank oversight.

- Impact on Import Bill Structures: Because crucial commodities like crude oil are priced in foreign currency, a lower domestic exchange rate inherently raises the landed cost of imports, creating upward pressure on wholesale and consumer price levels.

- Corporate Liquidity Dynamics: Extended periods of net selling compress corporate market capitalizations and reduce historical foreign ownership density across key financial and banking indices.

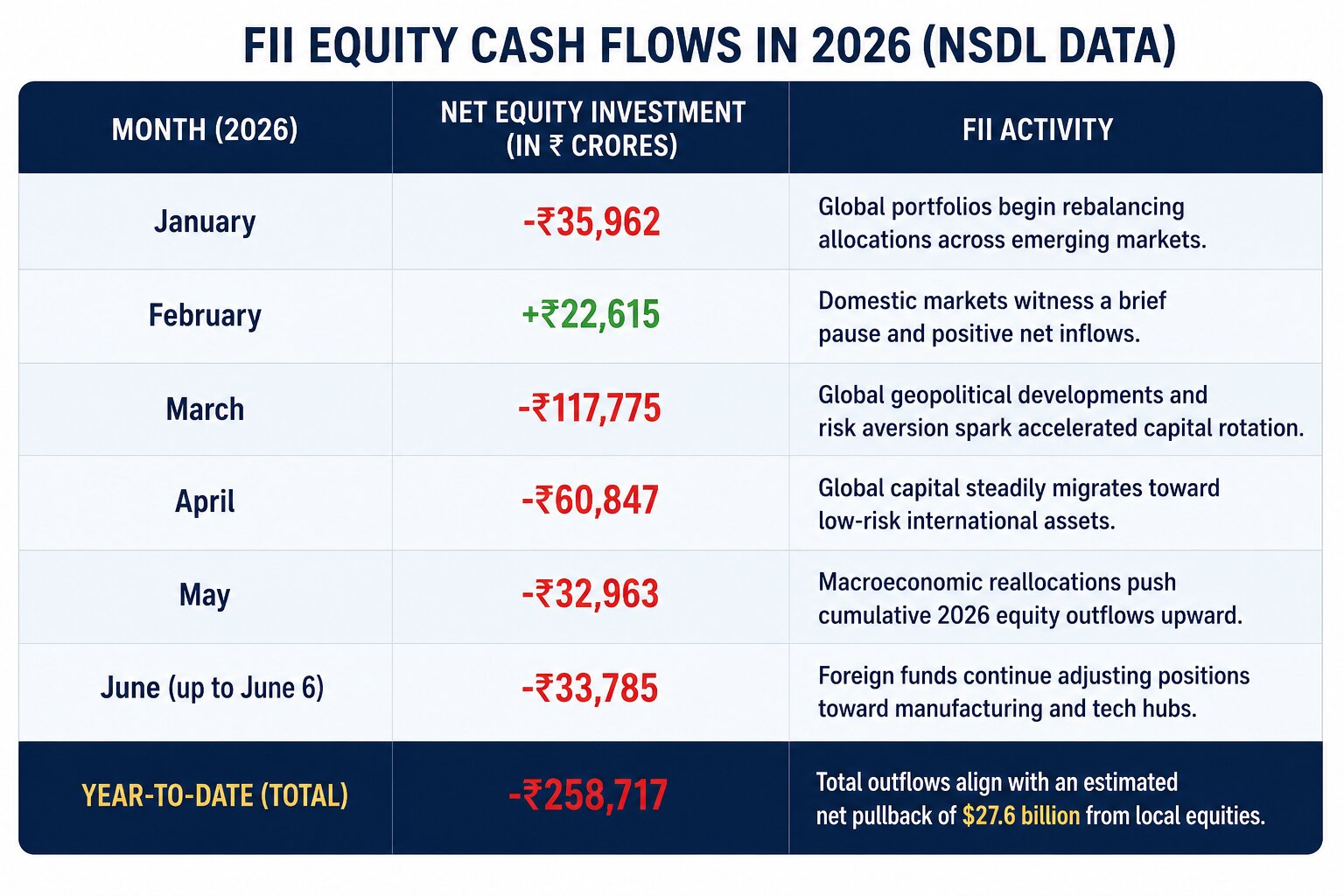

The Shift in Foreign Portfolio Flows (The NSDL Context)

The timing of this dual policy update aligns with recent capital movements recorded across domestic financial markets. Data from the National Securities Depository Limited (NSDL) highlights that foreign portfolio investors (FPIs) have been net sellers in the domestic equity cash segment this year, showing a preference for shifting capital across international regions:

Decoding the Response: The Joint Fiscal and Monetary Framework

To provide a stable counterweight to these equity outflows, fiscal and monetary authorities implemented a dual-action policy approach. While the Monetary Policy Committee (MPC) maintained a neutral stance and kept the policy repo rate unchanged at 5.25%, substantial modifications were made to the foreign investment code.

1. The Fiscal Channel: Targeted Sovereign Debt Exemptions

The central government promulgated the Income-tax (Amendment) Ordinance, 2026, amending Schedule IV of the Income-tax Act, 2025. This legislative update completely exempts Foreign Institutional Investors (FIIs) and the Bank for International Settlements (BIS) from income tax on interest income and capital gains earned from Government Securities (G-Secs). The ordinance is structured to take effect from April 1, 2026, seamlessly covering the current fiscal year.

By removing the standard 20% withholding tax on interest, alongside the 30% short-term and 12.5% long-term capital gains levies on debt assets, market analysts project net post-tax returns on Indian sovereign bonds will improve by 15% to 20%. This significantly builds the investment case for India's growing weightage in global sovereign bond indices, where passive tracking inflows remain highly resilient.

2. Central Bank Structural Calibrations

To maximize the impact of the tax exemption, RBI Governor Sanjay Malhotra announced major structural adjustments to minimize operational friction for international fund managers:

- Removal of Restrictive Investment Caps: For FPIs investing via the standard General Route, the central bank has permanently dismantled short-term investment limits, individual security caps, and portfolio concentration limits to maximize operational flexibility.

- Consolidation of Sovereign Investment Limits: The complex, separate sub-limits for ‘general’ and ‘long-term’ debt tranches have been merged into single, unified limits. For the 2026-27 fiscal year, the central government securities limit stands at ₹4,62,490 crore for the first half and ₹4,77,006 crore for the second half.

- Expansion of the Fully Accessible Route (FAR): The list of securities exempt from quantitative investment restrictions has been expanded to include all newly issued 15-year, 30-year, and 40-year government bonds, alongside Sovereign Green Bonds (SGrBs).

- Short-Term Capital Optimization: To support near-term foreign currency reserves, the RBI introduced a temporary concessional foreign exchange swap facility until September 30, 2026, for public sector undertakings utilizing external commercial borrowings. Simultaneously, the central bank will absorb full hedging costs for commercial banks raising fresh 3-to-5-year FCNR(B) deposits. Furthermore, the mandatory timeline for exporters to repatriate overseas proceeds has been shortened back to 9 months from 15 months.

- Broadening Equity Access: To cushion secondary markets, the RBI expanded equity investment access, allowing foreign individual investors to trade on local exchanges under limits identical to Non-Resident Indians (NRIs) and Overseas Citizens of India (OCIs) without separate registration hurdles.

The Strategic Objective: Prioritizing Institutional Capital

The long-term goal of this policy shift is to alter the foundational characteristics of inbound foreign capital. Public equity investments operate as highly liquid flows that react instantly to shifting global sentiments. In contrast, institutional debt capital from global pension systems and sovereign funds remains inherently long-term and stable.

By channeling global liquidity directly into 30-year and 40-year sovereign infrastructure and green bonds, the economic leadership is building an effective buffer. Leading financial economists expect these synchronized steps to help bridge the estimated $40 billion to $50 billion balance of payments gap for the fiscal year, funding long-term national development goals while maintaining standard currency stability.

Bottom Line

The 2026 coordinated updates mark an important milestone in the maturation of India's capital infrastructure. By easing the tax and regulatory rules that historically insulated the domestic sovereign debt market, the country is cultivating a deeper capital base. The ultimate success of this macro strategy will rest on the central bank's ongoing capacity to absorb global debt dynamics while maintaining reliable domestic liquidity.