Will Username Features Break India's Fintech Ecosystem?

India’s regulatory crackdown on username-based privacy features in apps like WhatsApp and Telegram signals a looming collision between digital anonymity and the country's phone-number-dependent financial backbone. As regulators demand traceability, the future of private messaging in India hangs in the balance.

Photo by Pixabay on Pexels

Will Username Features Break India's Fintech Ecosystem?

India’s regulatory crackdown on username-based privacy features in apps like WhatsApp and Telegram signals a looming collision between digital anonymity and the country's phone-number-dependent financial backbone. As regulators demand traceability, the future of private messaging in India hangs in the balance.

The Regulatory Collision Course

The Indian government has officially signaled its intent to tighten its grip on how digital identities are formed. Recent notices issued to WhatsApp, Telegram, and Signal suggest that the era of 'hidden identities' on messaging platforms is facing a severe reality check. At the heart of this friction is the government’s concern that username-based contact discovery—a feature designed to offer users privacy by hiding their phone numbers—creates a 'black hole' for law enforcement.

Regulators argue that in the context of national security, traceability is non-negotiable. While platforms view usernames as a tool to prevent doxxing and harassment, the Ministry of Electronics and Information Technology (MeitY) appears to view them as a digital mask that facilitates illicit activities. By decoupling the account from the verified mobile number, these apps are seen as potentially bypassing the existing identity verification loops that the state has spent years codifying.

"Privacy isn't a bug; it's a feature. If we lose the ability to contact people without exposing our financial-linked phone numbers to every stranger in a group chat, we are basically handing over our digital life to spammers and state surveillance." — @TechPrivacyIndia, X

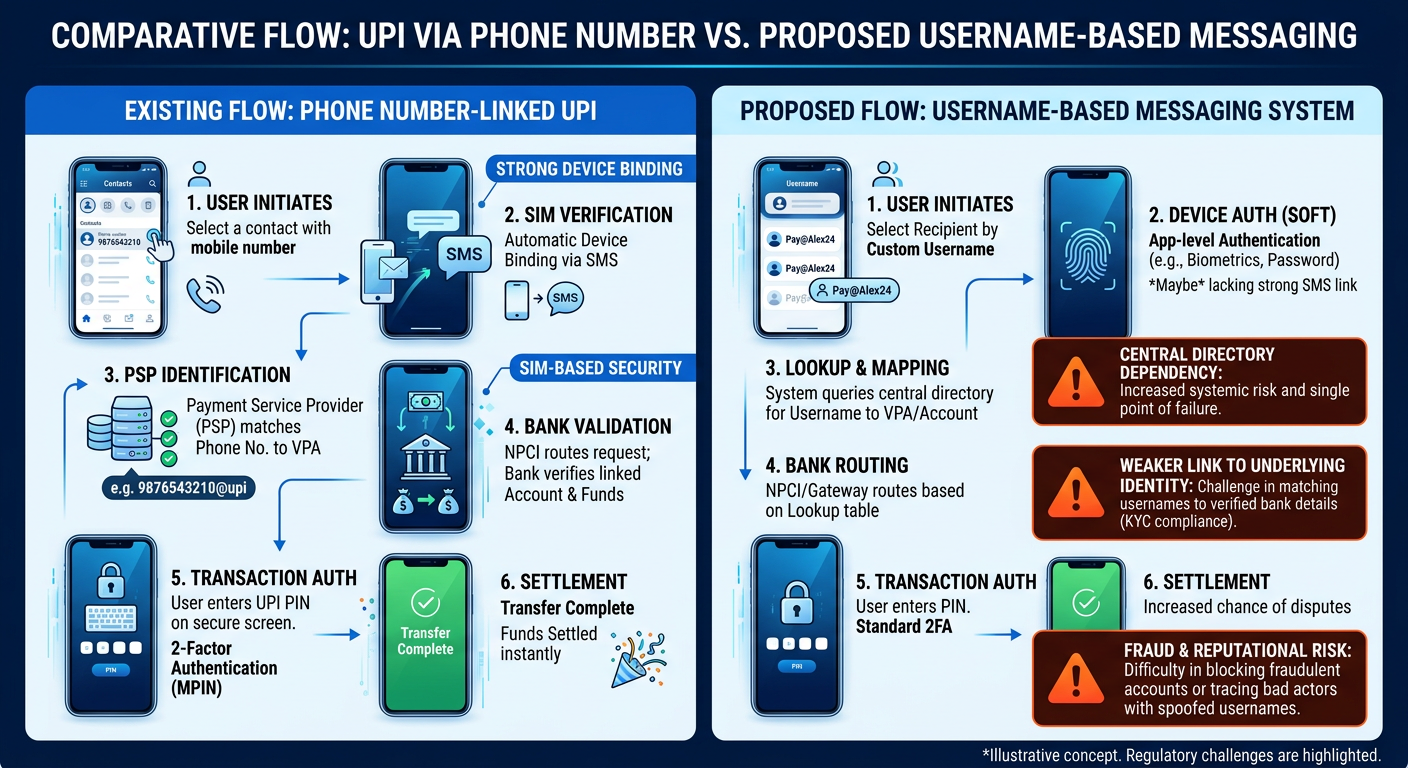

Threat to the UPI Backbone?

The risk here is not just about messaging; it is about the fundamental architecture of the Indian economy. India’s Unified Payments Interface (UPI) is built on a bedrock of trust and traceability where the mobile number serves as the immutable anchor. When you send money, you are sending it to a verified digital identity tethered to a bank account via telecom authentication.

If messaging platforms transition to decentralized, username-based architectures, they create a 'fragmented identity' ecosystem. If a user can initiate a transaction or a commercial interaction through an unverified username, it disrupts the KYC mandates enforced by the Reserve Bank of India (RBI). The fear is that if communication moves away from verified phone numbers, it creates a loophole for 'identity-as-a-service' threats where bad actors could hide behind non-KYC-compliant handles to conduct financial fraud.

Safety vs. Surveillance: The Debate

Privacy advocates argue that usernames are the only shield against a growing epidemic of identity theft and harassment. When your phone number is your identity, it is inevitably leaked in data breaches, leading to a constant deluge of spam and phishing. Proponents of usernames claim the government's focus is misdirected; phishing and impersonation occur today on phone-number-linked platforms regardless of privacy settings.

Conversely, the state maintains that 'lawful access' is a prerequisite for a safe digital society. The conflict mirrors debates seen in the UK regarding the Online Safety Act. Is the weakening of end-to-end encryption or the forced linkage of accounts to government-verified IDs worth the trade-off in security? Experts are divided, with many suggesting that mandating traceability inherently introduces backdoors that could be exploited by malicious actors, not just the state.

What Comes Next: Bifurcation or Compliance?

As the pressure mounts, messaging giants are faced with a stark choice: build a 'Verified Local Mode' specifically for the Indian market or risk losing access to one of their largest user bases. We may see a transition toward Sovereign Digital Identity, where services like ABHA or DigiLocker act as the bridge, validating users without platforms needing to store raw mobile numbers.

Will companies like Telegram and Signal—platforms famously built on anonymity—bend to these requirements? The cost of compliance is high, but the cost of exiting the Indian market is higher. We are likely heading toward a bifurcated internet where the 'Global Anonymous Mode' is swapped for a highly regulated, document-verified experience in India.

Bottom Line

India is attempting to reconcile the 20th-century need for physical traceability with the 21st-century reality of digital privacy. By linking the security of the financial backbone to the identity of the messaging user, the government is effectively turning every app into a KYC-compliant entity. Whether this preserves the security of our payments or merely erodes the freedom of our communication remains the defining digital debate of the decade.